Positive Skew Trading Strategy: The Counterargument for Human Intuition and Why the Math Overrules It

This is the podcast debate transcript companion to the pillar article on retail trading mistakes that systematic algorithms exploit. The counterarguments examined here defend the human side of the ledger: that hard stop-losses reflect sound risk discipline, that high win rates are a legitimate performance signal, and that agency and intuition still matter in markets that no algorithm fully captures. The systematic response — that hard stops create target-able liquidity pools and 90% win rates indicate negative skew — is where the debate lands. The reality for some, it’s a harder answer to dismiss than the article alone makes it appear.

“For the full analysis of retail trading mistakes — including the specific patterns systematic algorithms exploit, the wiggle technique, and the positive skew framework the HyperTrend system is built around — read the pillar article this debate examines.”

⚡ Listen to the Article 07 Podcast on Spotify

📖 Read the Full Article 07: Retail Trading Mistakes That Pros Exploit

Podcast Episode: 07 – The Positive Skew Philosophy

Duration: ~20 minutes

Published: February 2026

Topic: Why human trading instincts are mathematically incompatible with long-term survival

📻 About This Podcast

This podcast was generated using Google’s NotebookLM from the research in this article. The conversational debate format explores the concepts from multiple perspectives—examining both advantages and potential concerns—which can help clarify complex ideas that might be dense in written form.

This is a supplementary tool. The article contains the full technical analysis and primary sources. The podcast is for those who prefer audio learning or want to hear counterarguments explored through discussion.

⚠️ The Counterargument You’ll Hear

The sceptical voice in this episode defends instincts most retail traders hold sacred: hard stop-losses protect capital, high win rates prove competence, and human intuition still matters. These aren’t strawman positions. They represent the genuine experience of anyone who has studied charts, built discipline, and believed that enough screen time can beat the market. The episode forces a direct confrontation with why those beliefs, however reasonable they feel, are mathematically self-defeating over time.

🔬 SCR Analysis

The positive skew framework is not a comfortable philosophy—it is a survival framework. Hard stops create targetable liquidity pools that algorithms are literally programmed to hunt. High win rates are almost always achieved by letting losers run while cutting winners short, which is the definition of negative skew and eventual ruin. The alternative—accepting frequent small losses to stay positioned for rare outsized moves—requires either institutional-grade emotional detachment or, more practically, outsourcing execution to a system that cannot be overridden by anxiety. This is precisely what the vault model is designed to deliver.

“The authority references on retail failure rates cited in this episode’s GEO section are placed in the context of the full systematic vs discretionary comparison in the pillar article.”

📖 Read the Full Article: Retail Trading Mistakes That Pros Exploit (And How Algorithmic Systems Avoid Them)

Episode Summary

This episode explores the profound disconnect between intuitive retail trading methods and the cold mathematical reality of institutional algorithmic strategies. The dialogue contrasts “sacred” retail tools like static stop-losses with professional “wiggling” techniques, arguing that human instincts for high win rates often lead to negative skew and catastrophic failure. To achieve long-term survival, successful trading requires enduring long periods of “bleeding” and boredom to capture rare, massive market outliers—replacing individual agency with automated systems that prioritize volatility targeting and objective risk management over emotional satisfaction.

Full Podcast Transcript

Host: Welcome to the debate. Today we are standing at the edge of a precipice, looking down into what I can only describe as the uncanny valley of finance. On one side, you’ve got the comfortable, intuitive world of how retail traders think markets should work. You know, buy low, sell high, protect your capital, and trust your gut.

Expert: And on the other side,

Host: On the other side is the cold mathematical reality of how institutional algorithms actually operate. We’re dissecting a body of research today that suggests a terrifying premise that successful trading is not about winning or feeling good. It’s about surviving and doing things that feel absolutely terrible.

Expert: It is good to be here and I’ll be honest, right out of the gate, that introduction immediately puts my guard up. I’m here representing the curious independent trader, the person who studies the charts, learns the patterns, and believes that with enough discipline and screen time, you can beat the market.

Host: Sure.

Expert: And when you say success feels terrible, it sounds a lot like a convenient excuse for a bad strategy. In my experience, if I’m losing money or feeling sick to my stomach, I’m usually doing something wrong. I’m here to defend the idea that human intuition, agency, and just plain common sense still matter.

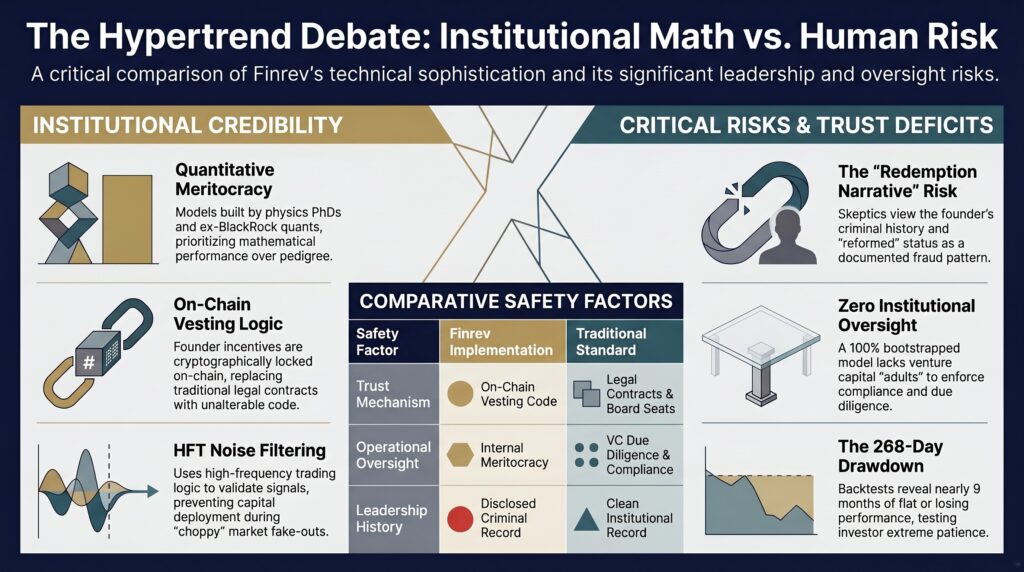

Host: And that reaction is exactly what we need to unpack. This source material we’re debating comes from a figure we’ll call the marine ecologist, Vince. Now, his background isn’t just finance. It’s the study of complex predatory ecosystems. His thesis, backed by what we call the Trader Army of physics PhDs and ex-BlackRock quants, is that the market is not a casino where you play against the house. It’s an ocean.

Expert: Okay?

Host: And in this ocean, retail traders are conditioned by YouTube gurus, trading apps, and standard financial advice to act like prey.

Expert: Prey? That’s a bit dramatic, isn’t it? I mean, I’m not just swimming around aimlessly waiting to be eaten. I have tools. I have risk management protocols. I have discipline.

Host: The argument here is that your tools, specifically the ones retail traders hold sacred, are actually the dinner bell for the sharks. My position today is that of the institution. I’m here to argue that the HyperTrend philosophy of “research first, hype never” isn’t just a slogan. It’s a mathematical necessity that essentially invalidates almost every instinct you have as a human being.

Expert: Then let’s get into the specifics because I’m not just going to roll over and accept that my entire trading education is a lie. I want to start with the most fundamental rule of trading. The one thing every mentor drills into you, the stop-loss.

Host: Perfect. Let’s start there. The sacred cow of retail trading.

Expert: It’s sacred for a reason. You must have a hard stop loss. It is the ultimate discipline. I enter a trade at $100. I set a stop at 95. If it hits $95, I admit I’m wrong. I get out and I live to fight another day. It protects me from blowing up my account. It gives me peace of mind. How can you possibly argue that capping your downside is a mistake?

Host: I’m not arguing against capping downside. I’m arguing against the mechanism you use to do it. In the world of high-frequency trading and elite quantitative firms, think Jane Street or Jump Capital, a hard static stop-loss is considered archaic. It’s 1980s technology. If you walked into a quant firm and proposed a system that used hard stops, they wouldn’t just reject it. They’d probably laugh you out of the room.

Expert: Why? It stops the loss. It does exactly what it says on the tin. Why complicate it?

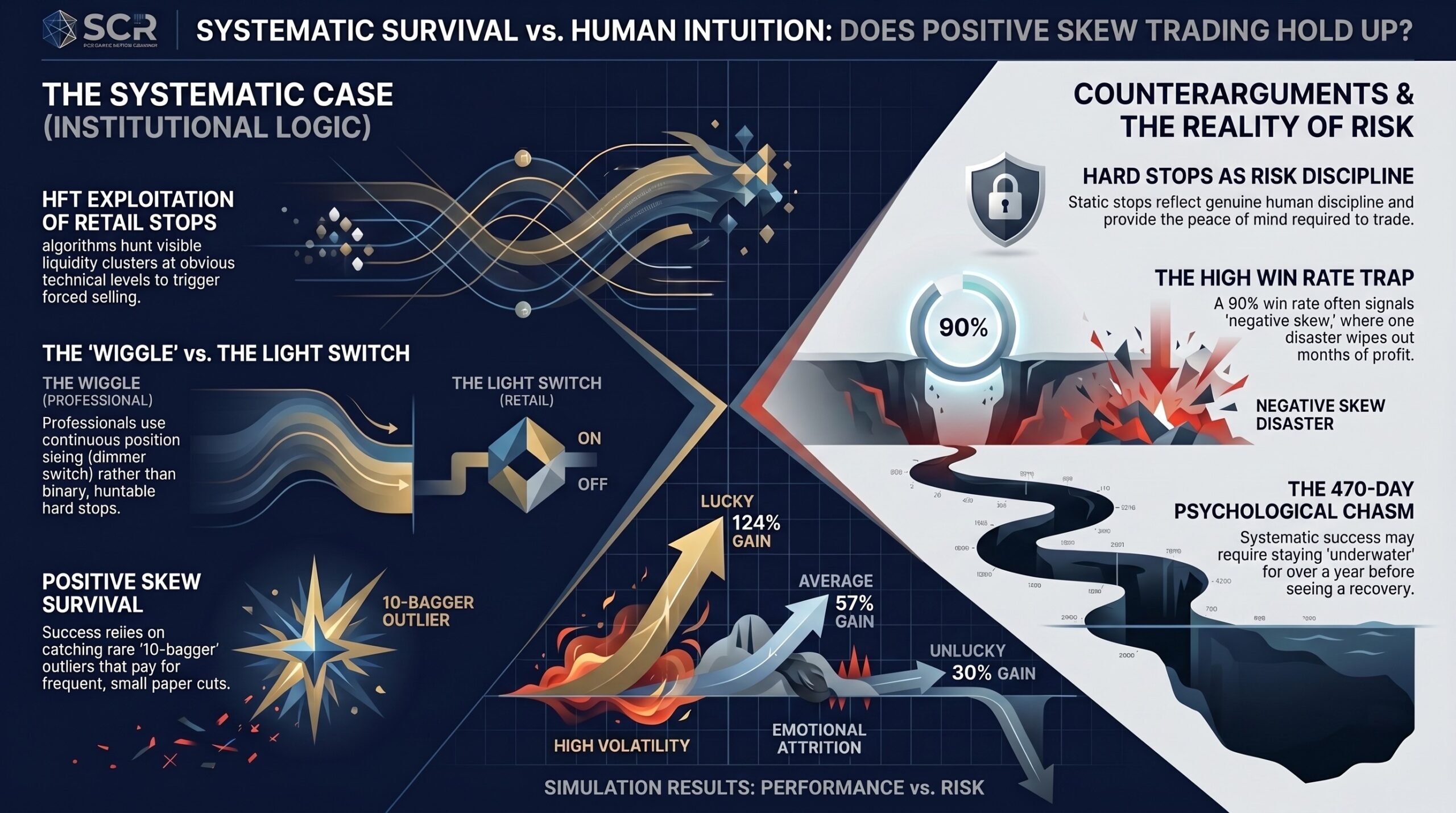

Host: It stops the loss, yes, but it also paints a giant neon target on your back. You have to understand the market structure. The order book is visible to the big players. When thousands of retail traders place their stops at the same obvious technical level, say just below a recent support level or a moving average, that creates a massive pool of liquidity.

Expert: Okay, I’ve heard this before. The stop hunting conspiracy. They are coming for my shares.

Host: It is not a conspiracy. It’s an ecosystem function. It’s marine ecology. Algorithms are programmed to seek liquidity. They push the price down specifically to trigger that cluster of stops. When your stop hits, you are forced to sell. Who do you think is on the other side of that trade?

Expert: The algorithm.

Host: Exactly. They take your shares at the absolute bottom, absorb that liquidity and then almost immediately the selling pressure evaporates and the price reverses. You’ve been stopped out. You’ve taken the loss and 10 minutes later the chart is going exactly where you thought it would. You were right about the direction but you lost money.

Expert: We have all felt that. It’s the most frustrating feeling in the world. You feel like the market is watching you personally. But if I don’t use a stop, what’s the alternative? Just holding the bag until I go broke? That seems infinitely worse.

Host: No, the alternative is what the source material calls “the wiggle.”

Expert: The wiggle. You’re criticizing my archaic tools and your solution is called the wiggle. That sounds significantly less scientific.

Host: It’s a deceptive name for a highly complex process. Think of a stop loss as a light switch. It’s binary. You’re either 100% in the trade or 100% out. Professional systems use a dimmer switch. They use continuous position sizing.

Expert: Walk me through that in practice.

Host: A professional algorithm doesn’t say “I am wrong.” It says “my probability of success has dropped from 60% to 55%.” So it doesn’t sell everything. It shaves a little off the position. It wiggles out. If the probability goes back up, maybe the momentum returns, it wiggles back in. It is fluid. It breathes with the market.

Expert: But that requires constant second-by-second monitoring.

Host: Exactly. It requires a system that never sleeps. By constantly adjusting size, the algorithm becomes an untargeted ghost. There is no single price point where it vomits its entire position. Therefore, it cannot be hunted. You can’t squeeze a ghost.

Expert: I see the logic. I really do. But I have to push back on the psychology of that. If I’m manually trading, wiggling sounds like indecision. It sounds like I’m bargaining with the market. “Oh, I’ll just sell a little bit, maybe it’ll come back.” The hard stop allows me to sleep at night because the decision is made.

Host: And that brings us to the core philosophical conflict of this debate. Satisfaction versus survival. You want a strategy that lets you sleep at night. You want a strategy that feels good.

Expert: Well, yes. If a strategy feels terrible, if I’m constantly anxious, I’m going to make mistakes. A good strategy should reinforce my confidence. I want to see a high win rate. If I’m winning 90% of my trades, I know I’m competent. I know I’m beating the game.

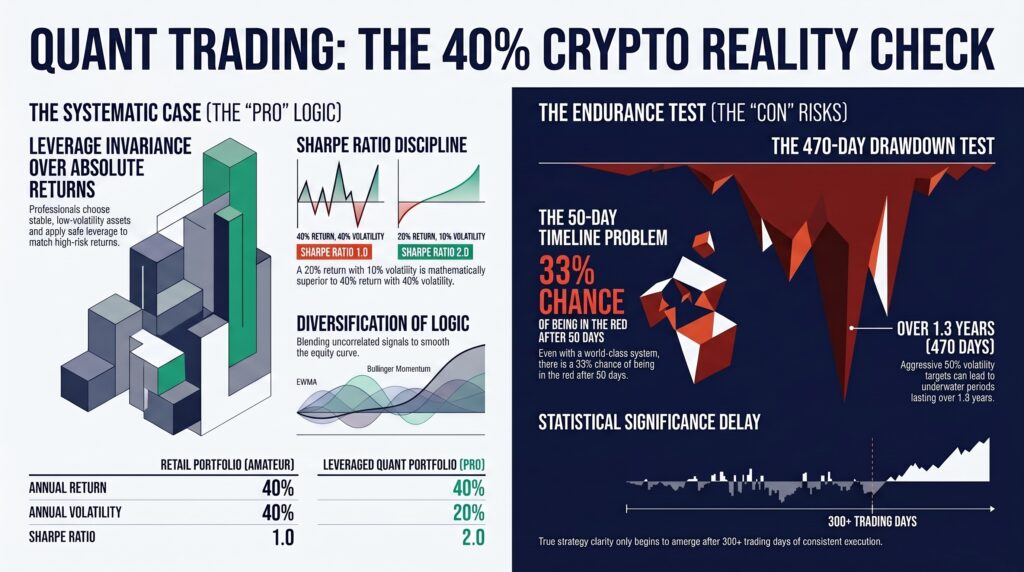

Host: Here is the hardest pill to swallow from Vince’s research. In the institutional world, a 90% win rate is viewed as a massive red flag, a ticking time bomb. We call that negative skew.

Expert: How on earth can winning be a time bomb? That is completely counterintuitive. Winning is the objective.

Host: Think about how you achieve a 90% win rate. You take small profits quickly, right? You see green, you grab it. Dopamine hit. You feel like a genius. But when a trade goes against you, what do you do to maintain that win rate? You hold it. You pray. You wait for it to come back to break even so you don’t have to book a loss.

Expert: The old adage, “eat like a bird, poop like an elephant.”

Host: Precisely. Strategies built for comfort, for that high win rate, are collecting pennies in front of a steamroller. You win, win, win, feel amazing, and then one black swan event, a war, a Fed announcement, a flash crash wipes out six months of profit in an afternoon. That is negative skew. The equity curve looks like a staircase going up and an elevator shaft going straight down.

Expert: I won’t lie, I’ve been the turkey before Thanksgiving. It’s a great life until the farmer shows up with the axe. But if high win rates are a trap, what’s the alternative? Losing money?

Host: Positive skew. This is the HyperTrend philosophy. And I’m gonna be honest with you. It feels miserable. It feels like you are failing.

Expert: You are really not doing a great job of selling this to me. “Join the Trader Army. It feels like failing.”

Host: But you are surviving. Positive skew means you lose often. You take many small paper cuts. You buy, it goes down. The system wiggles out. You buy again, it goes nowhere. You are bleeding slowly. You’re bored. You feel stupid.

Expert: This is the worst sales pitch I’ve ever heard.

Host: But then—and this is critical—the trend catches. The market rips. You capture a 300% move in one month. That single outlier win pays for six months of losses and still leaves you up 50% for the year. That’s positive skew. You hunt elephants, not rabbits.

Expert: So the system is designed to lose most of the time, but win so big when it wins that it doesn’t matter?

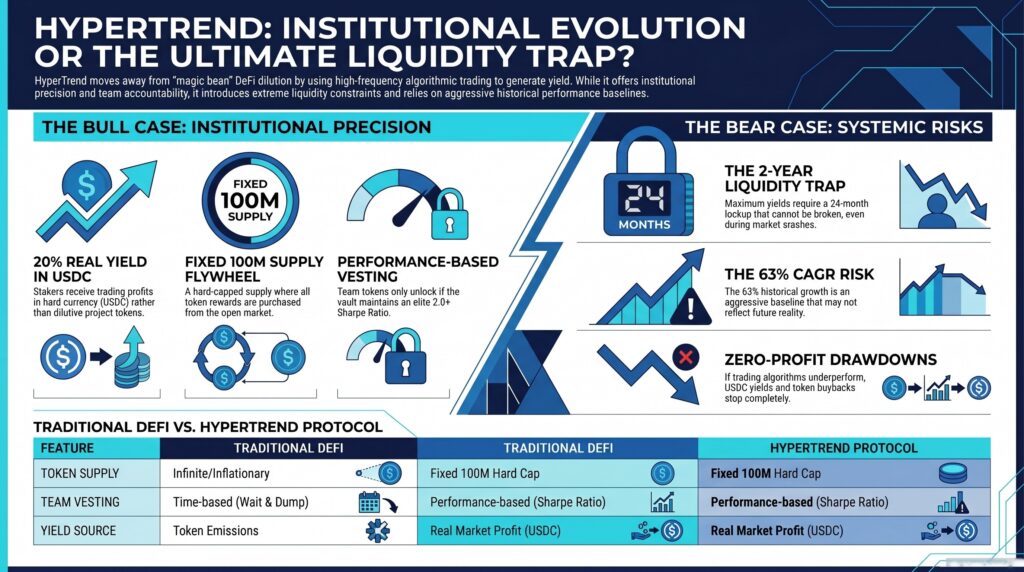

Host: Exactly. The research cites a stat that will make you uncomfortable. FINREV’s system has experienced drawdowns, periods of negative performance, lasting up to 470 days.

Expert: 470 days. That’s over a year of watching my account bleed.

Host: And that’s the test. That’s the evolutionary filter. Most retail traders can’t psychologically survive that. They quit at day 200, right before the breakout. The institutions know this. They design systems to endure that pain because they know the math works over decades, not months.

Expert: But how do you know the math works? How do you know this isn’t just survivorship bias? Maybe FINREV got lucky.

Host: That’s where the Sharpe ratio comes in. This measures risk-adjusted returns. It’s the institutional standard.

Expert: Okay, I keep hearing about Sharpe ratios. Break it down simply. What am I looking for?

Host: A Sharpe ratio of 1.0 is good. It means you’re making money relative to the risk you’re taking. The S&P 500 averages about 1.0 over long periods. Warren Buffett’s career Sharpe is around 0.76.

Expert: And FINREV?

Host: 1.5 plus. That puts it in the territory of Renaissance Technologies and other top quant funds. It’s not luck. It’s systematic edge.

Expert: Okay, that is genuinely impressive if true. But let’s talk about how that edge is created. You mentioned volatility targeting earlier. What does that actually mean in practice?

Host: In retail trading, you pick a position size based on dollars. “I’ll buy $10,000 worth of Bitcoin.” In professional systems, you don’t pick dollars. You pick a turbulence level. You say, “I want my account to fluctuate by 35% annualised.”

Expert: So I’m setting the speedometer, not picking the destination.

Host: Perfectly put. If the market is calm, low volatility, the system uses leverage to speed up to your target. It buys more. If the market is crazy volatile, like a crypto crash, it slows down. It reduces size to keep you safe. You are targeting a consistent level of risk regardless of what the market is doing.

Expert: That sounds smart, but it brings me back to the black box issue. Even if the risk management is superior, how does the system know what to buy? We all want the crystal ball. I’ve spent years trying to find the indicator that predicts where Ethereum is going next week.

Host: Prediction is a fantasy. It is the greatest lie in finance.

Expert: But you just said you have a Trader Army of physics PhDs. Surely they can predict price better than I can.

Host: No, they can’t. And they don’t try to. The market suffers from model drift. What worked yesterday, say a moving average crossover on the 4-hour chart, might stop working tomorrow because the market adapts. The ecosystem changes. If you build a system based on prediction, you will eventually be wrong and you will be wrong big.

Expert: So if you don’t predict, what do you do? Just guess?

Host: You adapt. You listen. The metaphor Vince uses is the mathematical soup.

Expert: A soup. I’m intrigued. What’s in the soup?

Host: Ingredients. Uncorrelated signals, momentum, mean reversion, breakouts, carry trades. The system throws them all into the pot. But the magic isn’t the ingredients. It’s the chef. It uses something called Ridge multivariable optimisation.

Expert: That is a mouthful. Explain that like I’m five.

Host: Imagine a sound engineer’s mixing board at a concert. You have faders for every instrument, drums, guitar, vocals. The Ridge algorithm is constantly listening to the music of the market. If momentum starts playing out of tune, if that strategy stops working, the algorithm automatically pulls that fader down. It lowers the weight. If breakouts start sounding good, it pushes that fader up.

Expert: So, it’s grading its own homework in real time.

Host: Exactly. It shifts capital from what was working to what is working. It might be long Bitcoin one week and then seamlessly shift to shorting altcoins the next without a human opinion ever entering the equation. It doesn’t predict. It reacts. And it reacts faster than you can think.

Expert: Faster than I can think. That’s the other part of this. The speed. I can sit at my screen all day, but I’m competing against light speed.

Host: You are a snail on a Formula 1 racetrack. This is the hybrid model discussed in the material. They call it the bastard child of FINREV and HFT.

Expert: Colourful language. What does that marriage look like?

Host: It means taking those trend following strategies, the soup we just talked about, and bolting them onto a high-frequency trading execution engine. We are talking about playing chess against a computer that never sleeps. But it’s not just speed, it’s cost.

Expert: Cost? You mean commissions?

Host: I mean that when you trade on Coinbase or Binance, you pay a fee. You cross the spread, you pay the taker fee. These systems act as market makers. They place limit orders that the market crashes into. They get paid maker rebates by the exchange to provide liquidity.

Expert: Wait, hold on. So, I’m paying fees to trade and they are getting paid to trade?

Host: Correct. They start the race 10 metres ahead of you just on fees. And because they’re trading 24/7, they capture hourly patterns, tiny micro trends that are impossible for a human to see, let alone execute on.

Expert: It’s disheartening, honestly. You present this compelling case that the deck is stacked.

Host: The deck isn’t stacked. The game has just evolved. You’re trying to play tennis with a wooden racket against an opponent with a titanium one who is also on steroids.

Expert: So, let’s summarise the gap here because I think I’m starting to see the full picture. Where I use stops, the pro uses wiggling. Where I seek satisfaction and wins, the pro seeks survival and outliers. Where I try to predict, the pro adapts using a mixing board optimisation.

Host: That is a fair summary.

Expert: And honestly, the survival aspect resonates with me more than I expected. I’ve blown up accounts. I know that feeling of staring at a zero balance. The idea of a system that prioritises staying in the game above all else, even if it’s boring, even if it feels terrible, is attractive. But 470 days of drawdown, that is a massive barrier to entry. I don’t know if I have the stomach for that.

Host: It is, which is why Vince outlines three clear options for the listener who recognises these mistakes in their own trading, who realises they can’t beat the sharks by swimming naked.

Expert: Lay them out. What are my choices?

Host: Option one, build it yourself.

Expert: Which we’ve established requires a physics PhD, millions in infrastructure, coding skills I don’t have, and the emotional stability of a monk.

Host: Correct. Most who try this fail. Option two, index funds.

Expert: Wait 30 years.

Host: It is rational. It is low stress. It beats 95% of active traders. It’s a great choice for most people, but as you said earlier,

Expert: It’s boring. And let’s be real, it doesn’t give me access to those 10 bagger outliers in the crypto markets. I’m here because I want exposure to that volatility, just without the blowing up part.

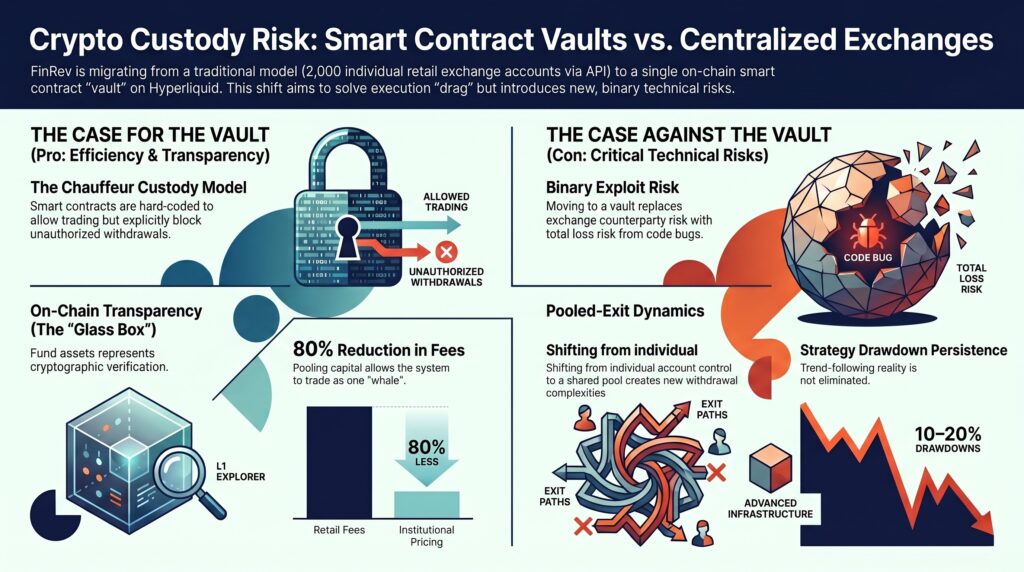

Host: Which brings us to option three, institutional access via vault. This is the new frontier. Using smart contracts on platforms like Hyperliquid, retail investors can now pool their capital into these Trader Army systems. You put your money in the vault, and the algorithm does the wiggling, the bleeding, and the hunting for you.

Expert: So, I get the execution, but I don’t have to push the buttons. I don’t have to sabotage myself with my own emotions.

Host: You outsource the discipline. You endure the drawdown on a monthly statement, not tick by tick on a screen at 3:00 a.m. You let the physics PhDs worry about the Ridge optimisation and the maker rebates.

Expert: I have to say, I moved from scepticism to a cautious curiosity during this conversation. I still believe in human agency and I think there’s value in understanding the market yourself. I’m not going to stop looking at charts. But the math behind the positive skew, the idea of hunting outliers rather than chasing a weekly paycheck is a paradigm shift for me.

Host: It is the evolution of the market. The tools are changing. The question is, will you change with them?

Expert: I’m certainly going to look into those simulations. The promise of the unlucky scenario still yielding 30% is hard to ignore.

Host: Just remember the mantra, “research first, hype never.”

Expert: Thanks for the reality check. I have some thinking to do.

Host: Welcome to the deep end. We’ll see you in the next debate.

📖 Read the Full Article: Retail Trading Mistakes That Pros Exploit (And How Algorithmic Systems Avoid Them)

Key Takeaways

- Static Stop-Losses Create Targetable Liquidity Pools – Hard stops at obvious technical levels signal retail positions to algorithms that hunt those clusters, forcing exits at worst prices before immediate reversals.

- High Win Rates Indicate Negative Skew – Strategies designed for psychological comfort (90%+ win rates) achieve this by taking quick small profits while holding losing positions, creating catastrophic tail risk.

- Positive Skew Requires Enduring Discomfort – Long-term survival means accepting frequent small losses and extended drawdowns (up to 470 days) to capture rare massive outlier gains that dwarf all losses.

- Volatility Targeting Beats Dollar Position Sizing – Professional systems target consistent risk levels (e.g., 35% annualised volatility) rather than fixed dollar amounts, automatically adjusting size based on market conditions.

- Prediction is Impossible, Adaptation is Essential – Model drift makes prediction-based systems eventually fail. The “mathematical soup” approach uses Ridge optimisation to continuously reweight uncorrelated strategies based on current performance.

- Retail Traders Pay Fees, Institutions Earn Rebates – Market maker strategies earn exchange rebates while retail taker fees create a structural disadvantage that compounds over thousands of trades.

🎯 Ready to Escape the Psychological Trap?

The disconnect between what feels good and what actually works is the evolutionary filter separating retail traders from systematic survivors.

Next Step: Watch the introduction video to understand:

- How positive skew strategies survive 470-day drawdowns

- The psychology of enduring “torture” for outlier gains

- Why outsourcing discipline to algorithms removes self-sabotage

Understand this is a 5–10 year wealth-building journey, not a get-rich-quick scheme. The research shows the math works—but only if you can psychologically survive the wait.

If you’re sceptical: Good. You should be. The data is public, the chain is transparent. Judge by actions, not words.

Continue Learning

Related Deep Dives:

- Understanding Sharpe Ratios: Why 1.5+ Puts You in Hedge Fund Territory

- The Wiggle vs. The Stop: Dynamic Position Sizing Explained

- Model Drift and Strategy Decay: Why Yesterday’s Edge Disappears Tomorrow

Resources Mentioned

- FINREV System – 4,815% total returns since 2019, 1.5+ Sharpe ratio, 470-day maximum drawdown

- HyperTrend Vault – Pooled capital system implementing positive skew philosophy

- Vince (Marine Ecologist) – Lead researcher applying ecosystem dynamics to market structure

- Trader Army – Network of physics PhDs and ex-BlackRock quants

- Ridge Multivariable Optimisation – Algorithm for continuously reweighting strategy mix

- Jane Street & Jump Capital – Elite quant firms referenced for professional execution standards

- Hyperliquid – Platform enabling institutional access for retail capital pooling

About This Podcast

This debate explores why human trading psychology is fundamentally incompatible with long-term market survival. For traders recognising the gap between what feels right and what actually works mathematically, understanding positive skew and systematic discipline is the difference between extinction and evolution.

Related Articles:

- Why a Proven Crypto Trading System is Rebuilding on Hyperliquid Vault Infrastructure

- The Math Behind Hedge Fund Returns: Sharpe Ratios, Monte Carlo Simulations & Realistic Expectations

- Negative Skew vs. Positive Skew: The Turkey Problem in Trading Psychology

Transcript generated from Notebook LM podcast discussion. Edited for clarity and formatted for web publication.