Table of Contents

🎧 Audio Discussion Available

An AI-generated podcast explores this article’s concepts through conversational debate format—useful for audio learners or those wanting to hear multiple perspectives.

Duration: 16 minutes

After three years of systematic research into professional crypto trading systems, I’ve identified a disturbing pattern: 5 critical retail trading mistakes are repeated over and over again. Almost everything retail traders believe about “good trading” is wrong. The truth is, I have been down this road more than once.

Not slightly wrong. Catastrophically, account-destroying wrong.

The delusions aren’t our fault. Commercial trading bots, YouTube gurus, and exchange marketing have conditioned retail traders to expect things that professional algorithmic systems intentionally avoid.

The result? Retail capital becomes the fuel that institutional algorithms extract systematically.

The emotional scars from watching “high win rate” systems explode, from being stop-hunted out of winning positions, from chasing returns instead of managing risk—those scars drove me to understand how professionals actually think about trading.

This article exposes five of those delusions by contrasting what feels good (retail thinking) with what actually works (institutional reality). Some of these truths will feel uncomfortable. That discomfort is the point.

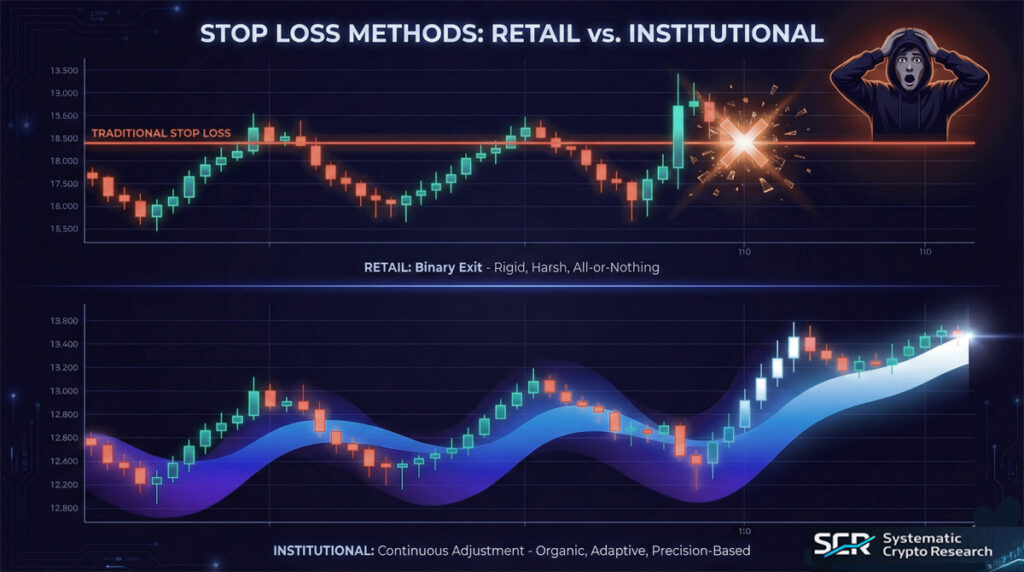

1. Stop Losses Are for Amateurs. Pros “Wiggle.”

Like most retail traders, I have used many strategies that rely on stop losses. It sounds completely logical to limit potential losses in this way. However, the reality is that because you are entering the trade at a predictable position, there are trading systems out there designed specifically to prey on your stop loss. So they get hit alarmingly often, and often the move against you goes straight to your stop loss and then reverses back in the direction you were trading. You have just been preyed upon. I don’t follow the herd anymore.

For the discretionary trader, the stop loss is a sacred tool—a pre-set price that automatically sells a position to cap a loss. It’s seen as a necessary discipline, drummed into us by every trading book and course. I certainly believed this for years.

But in the world of elite quantitative trading, the hard stop loss is a relic. Walk into a top-tier firm like Jane Street or Jump Capital and propose building a system with stop losses, and “they’ll just laugh at you and escort you straight to the door. It’s 1980s, 1990s technology.”

Professionals use a more fluid and capital-efficient method: a continuous signal that constantly adjusts, or “wiggles,” the position size. Think of it less like a light switch (on/off) and more like a dimmer dial, constantly adjusting the brightness based on the room’s conditions. As conviction in a trend increases, the algorithm adds to the position; as uncertainty grows or a reversal seems possible, it seamlessly scales back.

This approach aligns risk exposure perfectly with the system’s confidence—a far more sophisticated use of capital than a binary in-or-out decision.

Crucially, this dynamic sizing also inoculates the system against being stop hunted—a predatory practice where institutional players push prices to levels where they know retail stop-loss orders are clustered, triggering a cascade of forced selling they can absorb for profit. Without a single, predictable exit point, the professional system becomes an untargetable ghost.

As one institutional trader describes the process:

“I’m happy to be short here, but I’m not really confident yet… I’m getting more confident as the market’s going, I’m increasing my position… okay, now things are going good, now let’s get fucking real short and then as it looks like it might reverse, you want to be a bit cautious, take some off…”

This is position sizing as a continuous spectrum of conviction, not a panicked binary exit.

Stop hunting: Institutional players push prices to levels where they know retail stop-loss orders are clustered, triggering forced selling they can absorb for profit.

The problem with hard stops: They create a single, predictable exit point that sophisticated traders exploit. You get hit, market reverses, you just funded someone else’s profit.

The professional alternative: Continuous position sizing that “wiggles” like a dimmer dial—increasing allocation as conviction grows, decreasing as uncertainty rises. No binary exit point = impossible to hunt.

For the deep technical explanation of how signal-based position adjustment works through Ridge optimization and dynamic weighting, see Article 4: The Math Behind the Moonshots.

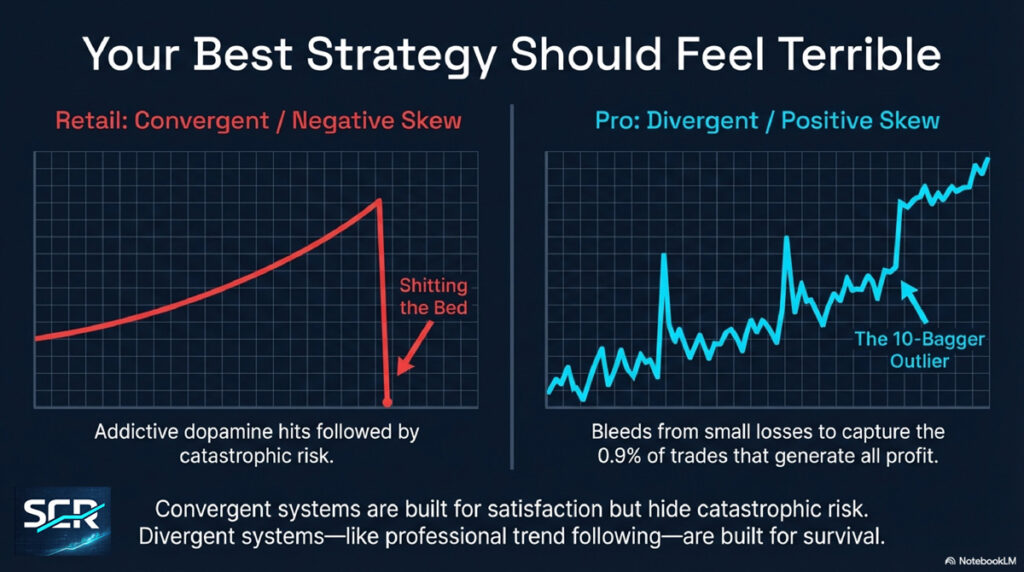

2. Your Best-Performing Strategy Will Often Not Look Like a Winner

One of the things that has always drawn me into trading and “trying” new indicators, setups, strategies, etc., is simply winning and thinking about winning big. And once you do it a few times, it is literally intoxicating. But there is an irony here, and that is simply to make those big or fast wins, you are taking big risks, and then it happens—the steady losses or big losses come. It’s not fun; in fact, it can be a heartbreaker. That is the story of most traders, however. I look at trading very differently now. I want to know more about the edge any trade or trading system has and the risk. The emotion of the big win is now kept in the past.

There’s a dangerous chasm between what feels good and what actually works. This is the fundamental conflict between two types of systems—a choice between “satisfaction” and “survival.”

Convergent, or “negative skew,” systems are built for satisfaction. Common among commercial trading bots, they feel fantastic to trade because they deliver a steady stream of small wins, creating a high win rate that makes you feel intelligent and in control. The dopamine hits are real and addictive.

The problem is the hidden, catastrophic risk. These systems are designed to make money consistently and then, without warning, “shit the bed,” wiping out months of gains in a few massive, unexpected losses that their backtests conveniently ignore.

I’ve traded these. They’re seductive. You feel like a genius… until you don’t.

Divergent, or “positive skew,” systems—the kind used by professional trend-followers—are built for survival. Trading them feels “like shit.” The account bleeds from many small losses and often goes sideways for agonizingly long periods. You question whether the system is broken. You’re tempted to abandon it for something that “works better.”

The entire strategy is a hunt for outliers. It endures the psychological pain to be correctly positioned for the rare, unpredictable market moves where, out of thousands of trades, just 0.9% become “10-baggers” that generate the lion’s share of all profits.

The ultimate paradox: the path of psychological endurance—survival—is the one that’s robust and built for long-term success in fundamentally unpredictable markets. Satisfaction is fleeting and often fatal. Survival is the only edge that matters.

| Feature | Negative Skew (Satisfaction) | Positive Skew (Survival) |

|---|---|---|

| Return Pattern | Frequent small wins → Rare catastrophic losses | Frequent small losses → Rare massive gains |

| Feels Like | Amazing! High win rate, you feel smart | Terrible. Constant small cuts, feels like bleeding |

| Backtest Appearance | Smooth upward curve (looks fantastic) | Flat…flat…SPIKE…flat…SPIKE |

| Reality | Selling insurance—you collect premiums until disaster strikes | Buying lottery tickets with positive expected value |

| Example | FTX perpetual carry trade (consistent…until it wasn’t) | Trend following (0.9% of trades generate majority of profits) |

The choice: Feel smart consistently then lose everything? Or feel dumb frequently then get rich eventually? Professionals choose survival.

For the full mathematics of positive skew, Monte Carlo simulations showing how drawdowns are features, not bugs, and why volatility targeting determines your experience, see Article 2: Why Crypto Hedge Funds Make 40%+ While Retail Traders Struggle.

3. “How Much Can I Make?” Is the Wrong Question

I was once in a trading group with a mentor who had amassed 250 million dollars trading huge leverage trades in the forex market on five-minute charts. I know this sounds like a tall tale, but it is not. I know his exact system, I traded it, and I watched him make 100% profit trades repeatedly. I spent the best part of a year trying to duplicate his success. There were 15 traders in our group. Only one mastered the strategy, and he made a lot of money. The rest of us tried very hard and failed. I learned a lot about trading and about myself in that journey. The trick here is that our mentor could execute these trades consistently at a 90% win rate, and we used a clever hedging technique to preserve a position long enough to get back on the right side of the trade if it went wrong. But you had to achieve perfect execution to do what our mentor could do. The one student who succeeded just happened also to be a champion poker player—this should give you a clue as to what it took to master this sort of trading. I mastered the mechanics and theory of this trade, but I was nowhere near mastering the mental game and the emotional game that went along with the ride of this sort of trading. Like I say, I learned a lot about myself.

Amateur investors obsess over a single metric: returns. We ask, “What percentage can I make?” I asked this for years, completely missing the point.

Professionals reframe the question entirely, shifting focus from an output they can’t control (returns) to an input they can (risk). They ask: “What return can I make relative to the risk I’m taking?”

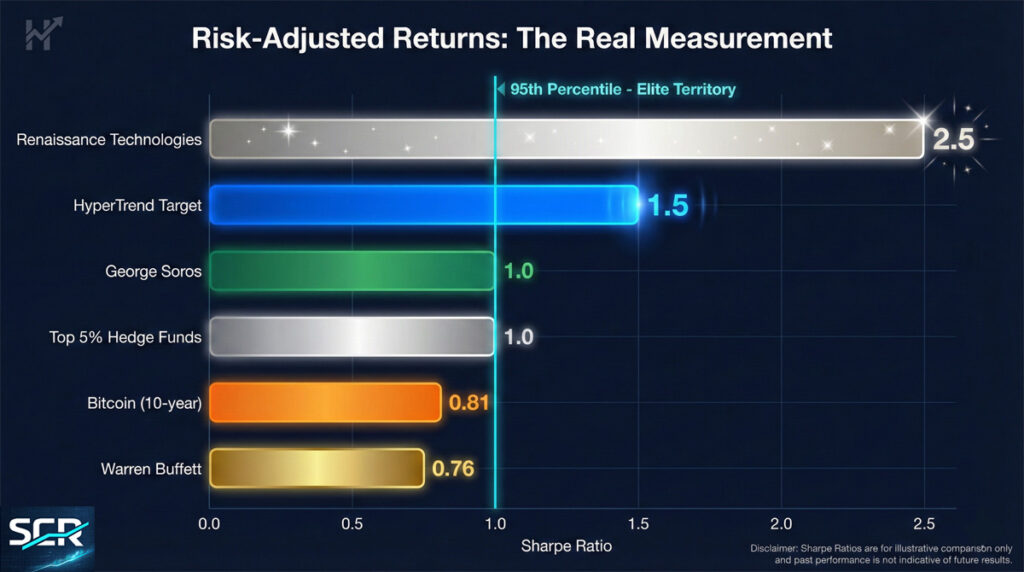

The industry’s yardstick for this is the Sharpe Ratio—described as the “quick and dirty way… to measure dicks” in the trading world. It’s a simple measure of return divided by volatility. A higher ratio means better performance for the amount of risk taken.

To put it in context:

- A Sharpe Ratio of 1.0 beats 95% of hedge funds globally

- Warren Buffett’s lifetime Sharpe is 0.76

- Simply holding Bitcoin for the last decade nets a 0.81

- HyperTrend targets 1.5+

Sharpe Ratio = Return ÷ Volatility. Measures how much return you get for each unit of risk taken.

Benchmarks that matter:

- 1.0 Sharpe: Beats 95% of hedge funds globally

- Warren Buffett: 0.76 lifetime

- Bitcoin (10-year hold): 0.81

- HyperTrend target: 1.5+

Why pros focus on this instead of returns: Risk is the dial you control. Returns are what the market decides to give you for taking that risk.

This philosophy leads to the core operational concept of volatility targeting. Users don’t choose a return; they choose a volatility target they’re comfortable with—how much their account balance “wiggles up and down”—and the system adjusts its leverage to maintain that risk level. The return is merely an outcome, heavily influenced by luck.

A simulation for a 35% volatility target reveals the stark impact of that luck:

- The Lucky Result: 124% per year

- The Average Result: 57% per year, but with a painful 47% drawdown that lasted 324 days

- The Unlucky Result: Still nearly 30% per year, but with a gut-wrenching 53% drawdown that lasted 470 days

Risk is the dial you control. Returns are what the market decides to give you for taking that risk.

Simulation: 35% volatility target (moderate risk) over one year

- Lucky outcome: 124% annual return

- Average outcome: 57% return, but 47% drawdown lasting 324 days

- Unlucky outcome: 30% return, but 53% drawdown lasting 470 days

What this reveals: Same system, same timeframe, wildly different experiences based purely on randomness. You need 12-15 months minimum to judge if a system actually works.

Why retail traders fail: They see someone’s “lucky 124%” and chase it right before regression to mean. Or they experience the “unlucky 53% drawdown” and quit right before the system works. Source: The Evaluation and Optimization of Trading Strategies (2nd Edition) by Robert Pardo

For full Monte Carlo simulations, Kelly Criterion position sizing mathematics, and a framework for choosing your personal volatility target, see Article 2: Why Crypto Hedge Funds Make 40%+ While Retail Traders Struggle.

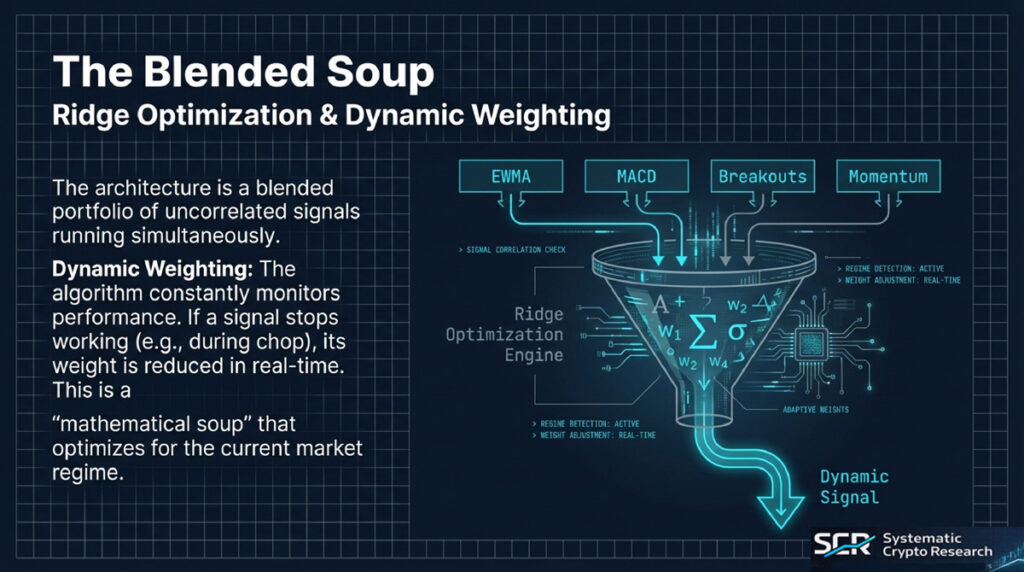

4. The Smartest Systems Don’t Predict—They Adapt

The holy grail of a perfect, static algorithm that has “solved” the market is a dangerous fantasy. I chased this for years, always convinced the next tweak would be the one that cracked the code.

Real-world strategies suffer from model drift—what once worked stops working as market conditions and participant behaviours evolve. The most robust systems, therefore, aren’t built to predict. They’re built to listen.

As the HyperTrend team describes it:

“What we’re doing is we’re not predicting the market at all. What we’re doing is listening to the market.”

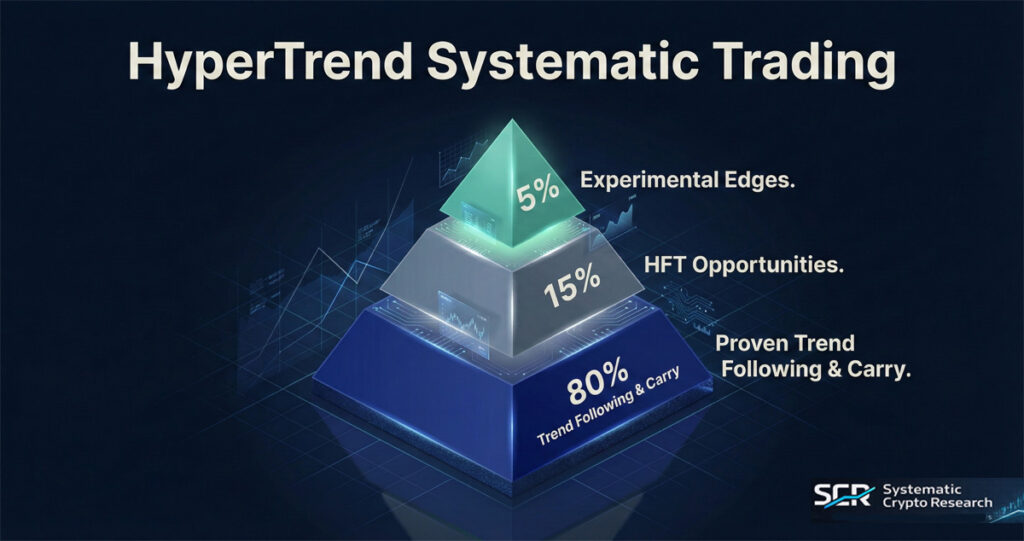

The architecture for this is a blended portfolio of multiple, uncorrelated trading signals—moving average crossovers, breakouts, momentum indicators, and others—running simultaneously. The true innovation lies in a dynamic weighting mechanism.

The algorithm constantly monitors the real-time performance of each signal. If moving average crossovers start to perform poorly in current conditions, the system automatically reduces their weight in the portfolio. Concurrently, it reallocates capital to the signals that are succeeding in the present environment.

This adaptive process was on full display during a recent crypto rally. When Bitcoin was leading the charge, the algorithm gave it significant portfolio weight. But as altcoins began to show stronger momentum, the system listened to that price action and automatically reduced Bitcoin’s weight, shifting capital to where the market’s actual strength was flowing.

This is not a prediction. This is disciplined, real-time adaptation to what’s actually happening rather than what you think should happen.

“What we’re doing is we’re not predicting the market at all. What we’re doing is listening to the market.”

How adaptive systems work:

1. Run multiple uncorrelated signals simultaneously (moving averages, breakouts, momentum, etc.)

2. Monitor real-time performance of each signal

3. Automatically reduce weight to signals degrading in current conditions

4. Reallocate capital to signals succeeding right now

Real example: During a crypto rally, Bitcoin got heavy weight. As altcoins showed stronger momentum, the system automatically shifted allocation to where actual strength was flowing.

Why retail can’t do this: Requires monitoring dozens of signals 24/7, making allocation decisions every second, without emotional override or fatigue.

For the deep technical explanation of Ridge multivariable optimization, how signal weights are determined through performance-based reweighting, and the “mathematical soup” approach to signal blending, see Article 4: The Math Behind the Moonshots

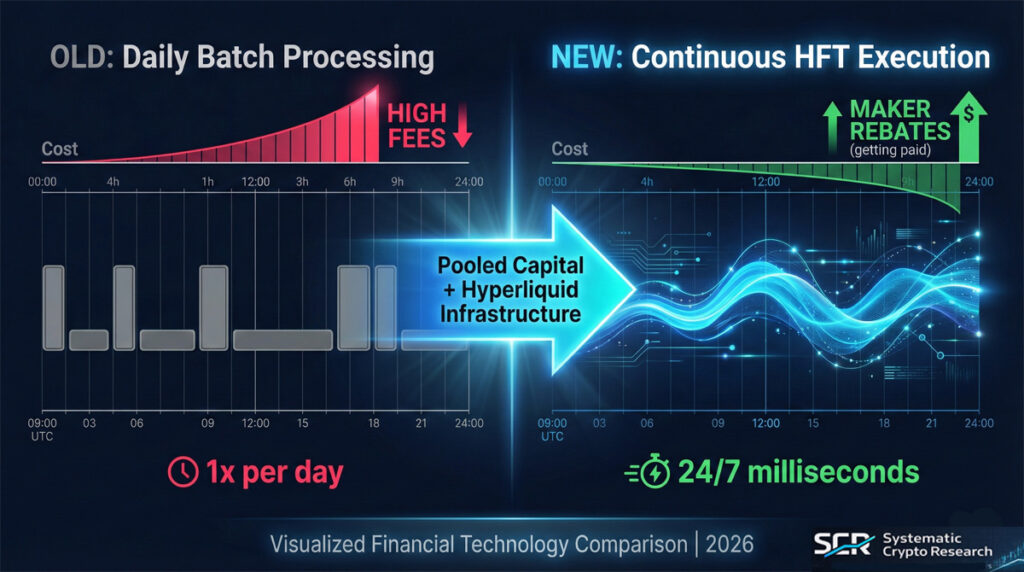

5. The Future Is a High-Speed Hybrid

Computers and AI systems can now outperform a genius-level world champion chess player. Would you like to bet you can outsmart a well-constructed computer program? And it works 24 hours a day in the crypto markets. Well, this is what trading is like in today’s world. Worse, that computer system has a lightning-fast connection to the market, and you have a snail-paced connection to work with. Think about that. When I first looked at Finrev several years ago, I realized there was no contest, not even close. Finrev could run circles around me trading.

Even robust trend-following models have limitations. The older generation traded just once per day, a frequency dictated by high transaction fees on centralized exchanges. This meant they could only capture slow-moving, multi-week trends, leaving what insiders describe as a “rich vein of very, very profitable trading” from faster market patterns completely inaccessible.

Finrev’s evolution represents a paradigm shift from a reactive, batch-processing model to a proactive, continuous one. The breakthrough was creating the “bastard child of Finrev and a high-frequency setup” by bolting a High-Frequency Trading (HFT) execution engine onto proven trend-following strategies.

This hybrid architecture unlocks game-changing advantages:

First: Trading costs plummet to near-zero. In some cases, by acting as a market maker, the system is actually paid to trade through maker rebates for providing liquidity to the order book.

Second: The system can trade constantly, 24/7, maintaining the exact portfolio exposures it desires at all times rather than being stuck with yesterday’s positions until tomorrow’s rebalance.

The consequence of this infrastructure is monumental. It unlocks a trove of previously inaccessible edges: hourly momentum patterns, pair correlations that play out over minutes not days, and mean-reversion opportunities on liquid assets. The resulting return profiles are smoother and more consistent—what traders dream of as “straight up and to the right.”

It bridges the gap between slow-moving trend systems and elite high-frequency firms, capturing the best of both worlds: the robustness of trend-following with the execution efficiency of institutional market-making.

For the full story of why HyperTrend rebuilt on Hyperliquid’s blockchain infrastructure to access pooled capital, VIP fee tiers, and HFT execution capabilities impossible with individual retail accounts, see Article 1: Why a Proven Crypto Trading System is Rebuilding on Hyperliquid.

Conclusion: The Systematic Edge Retail Can’t Replicate

Professional algorithmic trading operates on principles that directly contradict retail intuition:

- Continuous position sizing instead of stop losses

- Psychological endurance instead of satisfaction

- Risk management instead of return chasing

- Adaptive signal weighting instead of prediction

- High-frequency execution instead of daily batch processing

These aren’t just “better techniques”—they’re fundamental architectural differences that create an unbridgeable gap between institutional systems and retail traders manually executing on centralized exchanges.

The question isn’t whether you can learn these techniques. You can. The mathematics are published. The concepts are understandable.

The question is whether you can endure them psychologically when your account bleeds for six months waiting for the outlier move, or whether you’ll panic-sell at the bottom and switch to a “feels good” system that eventually explodes.

I couldn’t. I have the analytical capacity to understand these systems, but lack the emotional discipline to execute them manually. My psychology at some point betrays me every time. I suspect I’m not alone in this.

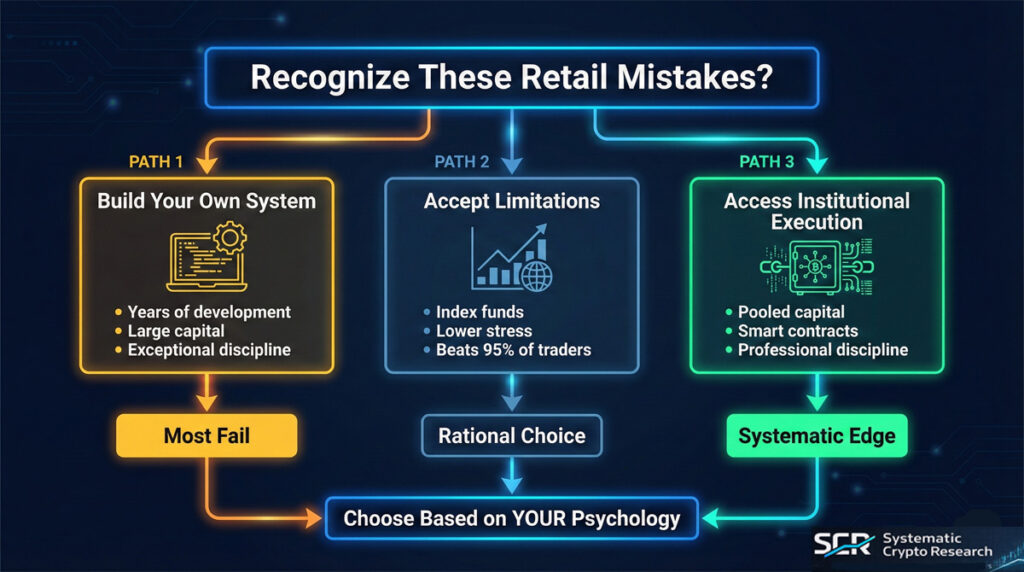

What This Means for You

If these truths resonate—if you recognize your own mistakes in this list—you have three options:

Option 1: Build your own system using these principles

- Requires years of development and backtesting

- Significant capital for live testing

- Exceptional psychological discipline

- Technical infrastructure (APIs, servers, monitoring)

- Most who attempt this fail

Option 2: Accept retail limitations and invest in index funds

- Nothing wrong with this approach

- Beats 95% of active traders over time

- Lower stress, lower time commitment

- Perfectly rational choice

Option 3: Access institutional execution through systems that implement these principles

- Innovative vault structures (like on Hyperliquid) pool capital for institutional advantages

- Smart contract custody eliminates counterparty risk

- On-chain transparency lets you verify everything

- You benefit from professional execution without needing professional discipline

I’ve chosen Option 3 after exhausting Option 1 for more than a decade. My trading taught me I lack the psychological makeup to master systematic execution, and I don’t want to spend my days in front of a screen. But I can research which systems embody these principles, verify their track records, and allocate capital accordingly.

This post may contain affiliate links

Next Steps: Are You Wanting To Know More?

- Click here to watch the special introduction video with Scott to learn more about HyperTrend, Finrev, and the process of becoming a member.

Understanding how professionals think is step one. Here’s how to go deeper:

- Meet the team building institutional-grade systems for retail access: Article 3: Inside the Finrev Team

- Deep-dive the mathematics of Sharpe ratios, volatility targeting, and positive skew: Article 2: Why Crypto Hedge Funds Make 40%+ While Retail Traders Struggle

- See the research methodology behind Ridge optimization and signal development: Article 4: The Math Behind the Moonshots

- Understand the tokenomics creating passive income from vault trading profits: Article 5: Trend Coin Tokenomics

- Learn the practical mechanics of depositing, point accrual, and wealth compounding: Article 6: HyperTrend Vault Launch Guide

The Final Question

Now that you’ve seen how professionals operate and exploit retail mistakes, what’s the single biggest assumption about your own trading strategy that you need to challenge?

Are you optimizing for what feels good, or what you hope for, or what actually works?

📄 Full Podcast Transcript: Why Winning Strategies Feel Like Failing

Questions or feedback? Reach me at contact@systematiccryptoresearch.com. I’m interested in your perspective and happy to discuss any aspect of this research.

Disclosure: This article discusses Finrev and HyperTrend systems. The author may have positions in the mentioned assets. This is educational content, not financial advice. Crypto trading involves substantial risk of loss. Past performance doesn’t guarantee future results. Team backgrounds and credentials don’t guarantee trading system performance. Do your own research and verify all claims independently.