Table of Contents

🎧 Audio Discussion Available

An AI-generated podcast explores this article’s concepts through conversational debate format—useful for audio learners or those wanting to hear multiple perspectives.

Duration: 16 minutes

If you’ve spent more than five minutes in the crypto world, you’ve probably seen the “Magic Bean” sales pitch. It usually involves a flashy car, a generic trading bot, and a promise that you’ll be retired by next Tuesday.

As a marine ecologist who spent decades creating marine protected areas and restoring habitats, I can tell you that nature doesn’t work like that—and neither do the markets. Complex systems—whether they are coral reefs or crypto exchanges—require a systematic approach, rigorous data analysis, and a healthy dose of humility.

For the last three years, I’ve been researching Finrev, an automated crypto trading platform, looking at it through the lens of a researcher rather than a promoter. My goal with this site is to document my transition from an amateur “textbook case” trader who ignored risk, to an investor looking for a state-of-the-art statistical definition of reward.

In this deep dive, we’re going to look at the professional-level research methodology that powers the new HyperTrend crypto trading signals and why the pedigree of the team—and the independent research I conduct here—is what separates a “bot” from an institutional-grade trading firm.

Who’s Behind This? (The 60-Second Version)

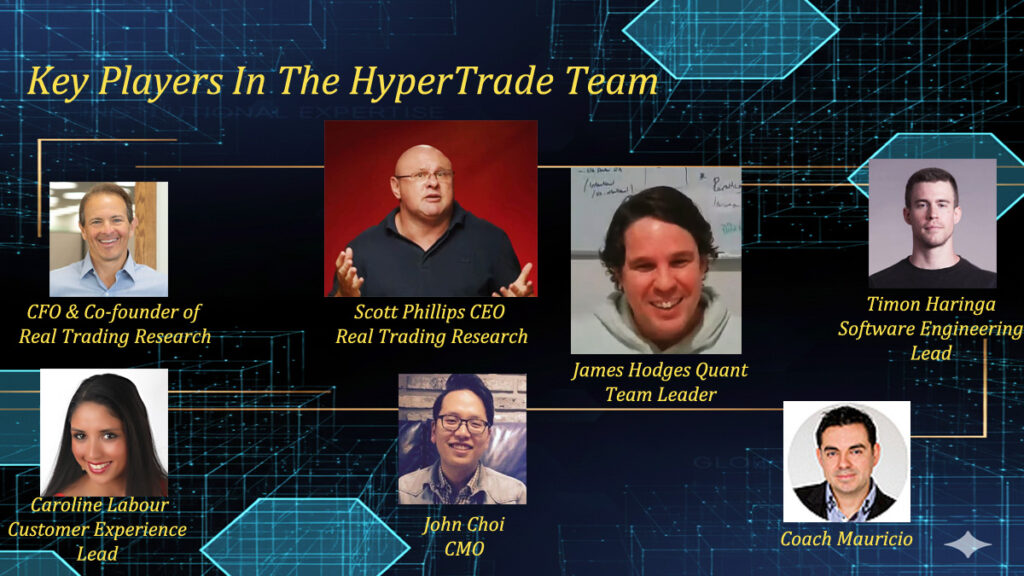

The research behind HyperTrend comes from a team with serious institutional pedigree: James Hodges (Physics PhD, ex-BlackRock quant) leads the quantitative research, while Scott Phillips (20 years trading, trained under legends like Van Tharp and Ed Seykota) brings hard-earned practical experience. Together with a 40-person “trader army”—most of whom Scott trained personally—they’ve built what is essentially a hedge fund operating in DeFi.

For the full story of how a hedge fund refugee and an ex-convict built this operation—including Scott’s redemption arc and why James left managing billions at BlackRock—see Inside the Finrev Team: The Hedge Fund Refugees and Ex-Convicts Building HyperTrend.

The Research Methodology: Ridge Multivariable Optimization

This is where HyperTrend separates itself from the “bot farms” you see advertised on YouTube. Most retail trading bots are built around a single indicator—maybe a moving average crossover or a RSI signal. When that indicator stops working (and it always does), the bot bleeds your capital slowly until you give up.

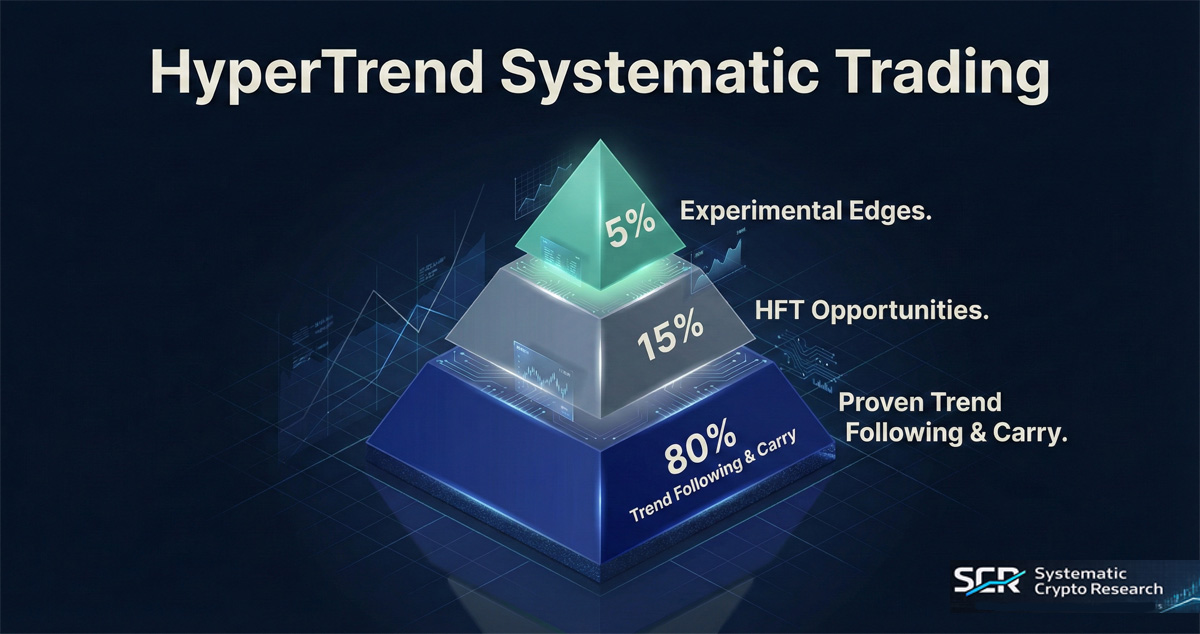

HyperTrend uses Ridge Multivariable Optimization, which sounds like academic jargon but is actually brilliant in its simplicity: instead of betting everything on one signal, the system blends 50 to 100 different “single variable” signals into a mathematical “soup.”

Ridge Optimization = Blending 50-100 different “single variable” trading signals into a mathematical “soup” where each signal gets weighted by its recent performance.

Why this beats single-indicator bots: Most retail bots rely on one indicator (moving average crossover, RSI). When that indicator stops working (and it always does eventually), the bot bleeds capital. Ridge optimization automatically reduces weight to degrading signals and reallocates to what’s working now.

The ingredients: Volume patterns, hourly reversals, lead-lag correlations, carry systems, breakout patterns, moving average dynamics—each tested across decades in traditional markets, adapted for crypto.

The Ingredients in the Soup

These signals include:

- Volume-based predictors: Is smart money accumulating or distributing?

- Hourly reversals: Short-term price dislocations that resolve quickly

- Lead-lag correlations: Does Bitcoin’s movement predict altcoin behavior?

- Carry systems: Funding rate arbitrage opportunities

- Breakout patterns: 320-day highs, multi-timeframe confirmations

- Moving average dynamics: Not just crossovers, but velocity and acceleration

Each of these signals has been tested across traditional markets—stocks, bonds, commodities—for decades. James isn’t inventing new magic; he’s applying what institutional quants have known works, adapted for crypto’s unique characteristics.

How the Weights are Determined

Here’s what makes this approach systematic rather than random: every signal gets a “weight” based on its recent performance, and these weights are recalculated regularly.

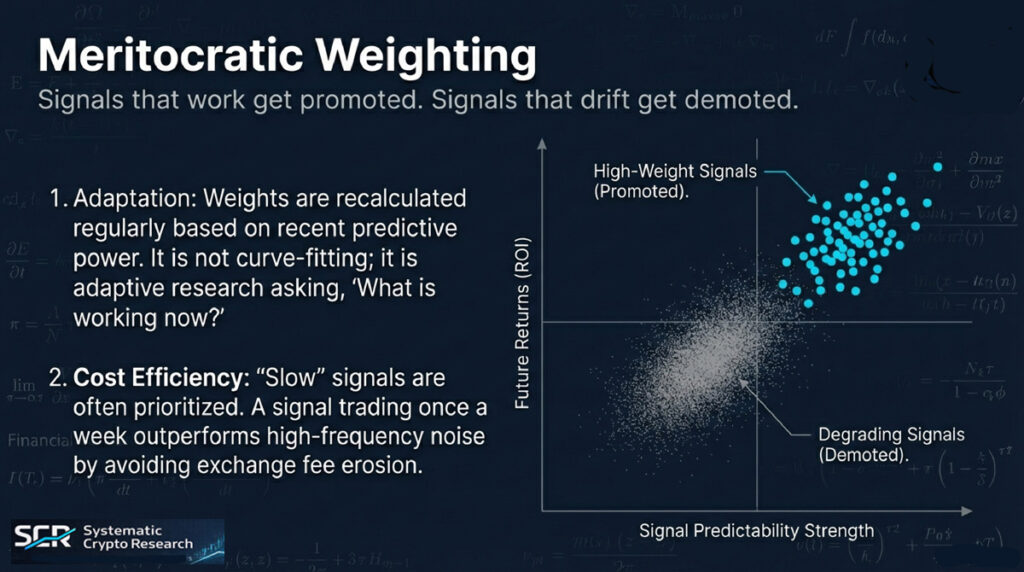

Performance-Based Reweighting: If a 320-day breakout signal is capturing profit in the current market regime, it gets more allocation. If a moving average crossover starts to “drift” or degrade—meaning its predictive power weakens—its weight is reduced automatically. The system is meritocratic: signals that work get promoted, signals that don’t get demoted.

Cost Efficiency Priority: One of James Hodges lead Quant’s key insights is that “slow” signals are often more profitable than “fast” ones, simply because exchange fees and slippage don’t eat your returns. A signal that trades once per week can outperform a signal that trades ten times per day, even if the latter has slightly better raw predictive power, because transaction costs matter enormously at scale.

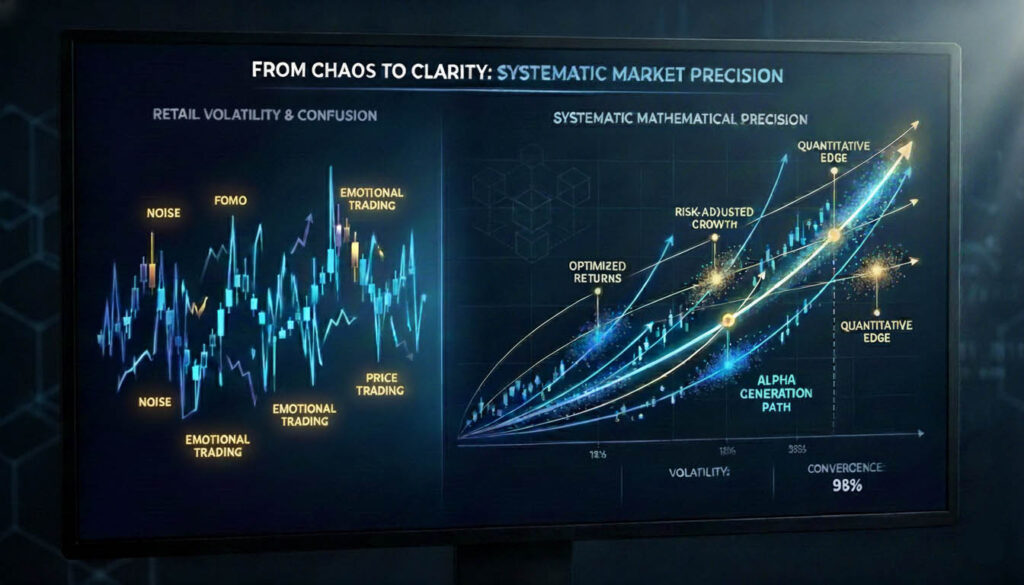

Professional trading systems use Ridge multivariable optimization to blend dozens of signals, each tested for predictive power across market conditions. This scatter plot illustrates how signal strength correlates with future returns.

This isn’t curve-fitting or over-optimization. It’s adaptive research—constantly asking “what’s working now?” while maintaining a foundation of strategies that have worked for over a century.

Counter-intuitive truth: A “slow” signal that trades once per week can outperform a “fast” signal that trades 10 times per day—even if the fast signal has slightly better raw predictive power.

Why: Exchange fees and slippage eat returns at scale. A signal that trades 10x daily pays fees 10x more often. Those costs compound dramatically over thousands of trades.

James Hodges’ key insight: When evaluating signals, cost efficiency is weighted equally with predictive power. A slightly less predictive signal with dramatically lower trading costs wins the allocation battle.

What retail traders miss: They optimize for “best prediction” and ignore that transaction costs can turn a theoretically profitable edge into a money-losing system in live trading.

The Criteria for “Tradable” Assets

You won’t find HyperTrend chasing the latest “Magic Bean” or a meme coin that launched two hours ago. The research protocol for adding new assets to the trading universe is strict and survival-focused:

The 365-Day Rule

A token must have at least one full year of trading history before the system will consider it. This filters out “IPO noise”—the wild volatility and manipulation that characterise newly launched tokens—and ensures there’s enough data to validate whether signals actually work on that asset.

The 5% Liquidity Filter

HyperTrend will never take a position that represents more than 5% of a coin’s daily trading volume or open interest. Why? Because exiting a large position in an illiquid market means you’re trading against yourself—your own selling pressure moves the price against you, turning paper profits into realized losses.

The Liquid Symbol Preference

Trend following works best on what the team calls “big stuff”—Bitcoin, Ethereum, Solana, and other high-cap, high-liquidity assets. These markets have enough participation that your edge doesn’t get arbitraged away instantly, and there’s always a counterparty when you need to exit.

This research-first approach prioritizes survival over satisfaction. It’s not about catching the 100x moonshot on a brand-new token. It’s about staying in the game long enough for the statistical edge to compound, knowing that a few large winners will pay for all the small losses and breakeven trades.

HyperTrend’s tradable asset criteria:

- 365-Day Rule: Token must have full year of trading history (filters out “IPO noise” and manipulation)

- 5% Liquidity Filter: Never take position >5% of daily volume/open interest

- Liquid Symbol Preference: Focus on “big stuff” (BTC, ETH, SOL, high-cap assets)

Why this matters: Research-first approach prioritizes survival over satisfaction. Not about catching 100x moonshot on new token—about staying in the game long enough for statistical edge to compound.

What’s filtered out: Brand new launches, low-liquidity altcoins, tokens with manipulation risk. These might 100x, but they can also trap you in illiquid positions where your own selling moves price against you.

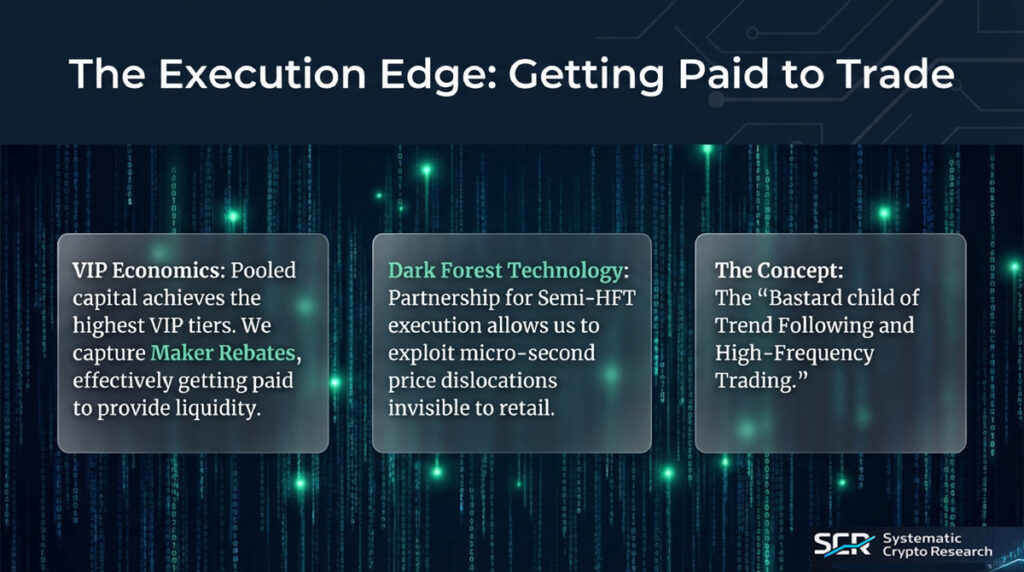

Why Rebuild on Hyperliquid? The Infrastructure Advantage

The transition from the original Finrev system to the HyperTrend vault on Hyperliquid was driven by research into execution efficiency. In the old model, Finrev managed thousands of individual trading accounts, which created execution lag and forced users to pay retail-level exchange fees.

By moving to a vault-based system, all member capital is pooled into a single institutional-grade account. This unlocks two massive advantages:

VIP Fee Tiers: Pooled capital means the vault operates at the highest volume tiers on Hyperliquid, often getting paid to provide liquidity rather than paying fees to take it. This edge compounds over hundreds of trades per month.

HFT Execution Partnership: Through a partnership with Dark Forest Technology, HyperTrend can execute trades based on short-term price dislocations—microsecond-level inefficiencies that retail traders can’t even see, let alone exploit. James describes this as the system “having sex with high-frequency trading,” and the result is better fills, tighter spreads, and fewer drawdowns.

For the full technical breakdown of why the team chose Hyperliquid’s Layer 1 architecture, smart contract custody model, and orderbook design, see Why a Proven Crypto Trading System is Rebuilding on Hyperliquid.

Risk Management: The Sharpe Ratio Target

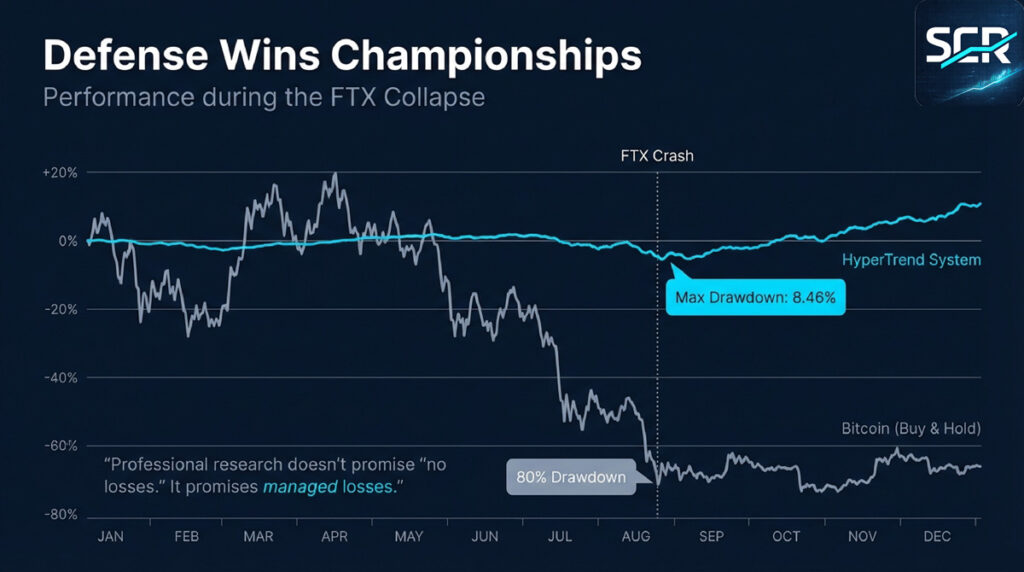

In my marine ecology work, I learned early that the average of a system tells you far less than its variance. A coral reef might look healthy on average, but if the variance is high—massive die-offs followed by recovery—the system is fragile.

Trading is the same. Professional research doesn’t promise “no losses.” It promises managed losses, measured using the Sharpe Ratio (returns ÷ volatility). A Sharpe of 1.0 puts you in the top 5% of hedge funds globally. Finrev’s historical Sharpe is 1.81. HyperTrend targets over 2.0—putting it in the same league as Renaissance Technologies, the greatest quantitative hedge fund in history, which runs at around 2.5.

During a 10-month testing phase that included the FTX collapse, HyperTrend’s maximum drawdown was just 8.46%. Compare that to Bitcoin, which has historically seen 80%+ drawdowns, and you see the value of systematic risk management.

Sharpe Ratio = Returns ÷ Volatility. Measures risk-adjusted performance.

The benchmarks:

- 1.0 Sharpe: Top 5% of hedge funds globally

- Finrev historical: 1.81

- HyperTrend target: 2.0+

- Renaissance Technologies: ~2.5 (greatest quant hedge fund in history)

Why this matters here: Professional research targets Sharpe ratios, not absolute returns. A 30% return with 10% volatility (3.0 Sharpe) is dramatically better than 60% return with 80% volatility (0.75 Sharpe).

Systematic trend-following strategies like HyperTrend target Sharpe ratios above 2.0 by managing volatility and limiting drawdowns. During the same market cycle where Bitcoin dropped 80%, trend-following systems maintained drawdowns under 10% through systematic risk management.

For the full breakdown of how Sharpe ratios work, why volatility targeting matters, and how the Kelly Criterion determines position sizing, see Why Crypto Hedge Funds Make 40%+ While Retail Traders Struggle.

My Independent Research Approach

I want to be crystal clear about my role here: I don’t work for Finrev or Real Trading Research. I am a paying member, an active investor, and yes, an affiliate who receives benefits if you join through my introduction. But I was a member before I became an affiliate, and I’d be tracking this data regardless of whether anyone else ever joined.

My background gives me a unique lens for evaluating this system. As a marine ecologist, I spent decades analyzing complex adaptive systems—understanding which variables matter, which are noise, and how to separate signal from randomness. But I also spent decades as a trader, and not a successful one.

In my limited spare time, I spent years chasing momentum strategies in Forex, obsessed with finding the indicator that would finally work reliably. I scored occasional big wins followed by crippling losses—a pattern I repeated in options and stocks, always leveraging a bit too hard and never fully understanding the risks. This is normal. It’s a fact that 90% of retail traders lose money—a staggering reality. Over time, automated trading has stood out as the way forward, especially now that technological advances in systems and analysis are accelerating each year.

Those years of manual trading taught me something crucial: humans are terrible at systematic trading. We get emotional after losses, overconfident after wins, and we constantly second-guess our own rules. Humans also get busy, tired, sick—life happens. In my case, there were times when I was literally underwater counting fish while unexpected market moves hit. My trades would be left hanging, accumulating losses. Automated systems don’t have these problems—but only if the research behind them is sound.

That’s why I now approach this as Research First, Hype Never. You’ll find detailed performance analyses on this site, including the 268-day periods where the Finrev system went sideways and nothing seemed to be working. I document the lumpy, bumpy reality of trend-following returns because that’s what actual research looks like—not cherry-picked equity curves and highlighted wins.

I’ve been a teacher at both high school and tertiary levels, and helping others understand how these systems work is genuinely more satisfying to me than just trading in isolation. Teaching forces clarity. If I can’t explain why a strategy makes sense, I probably don’t understand it well enough to trust my capital to it.

| Feature | Most Crypto Projects | Systematic Research |

|---|---|---|

| Performance Claims | Cherry-picked wins, hide drawdowns | Document 268-day flat periods, max drawdowns, “lumpy bumpy” reality |

| Team Background | Self-taught, no verifiable track record | BlackRock quant, trained by Ed Seykota/Van Tharp, 3-year live results |

| Strategy Development | Invented last month, no historical validation | Strategies proven across decades in stocks/futures, adapted for crypto |

| Risk Management | Promises “no losses,” “consistent returns” | Expects 10-20% drawdowns, 6-12 month flat periods, positive skew reality |

| Transparency | Backtests only, theoretical performance | On-chain verification, 2,000 live subscribers, auditable results |

The author’s role: Independent researcher, paying member before affiliate, documenting systematic analysis—not promotional marketing.

Conclusion: Systematic Thinking Over Emotional Trading

Most people in crypto are looking for the next 100x token or the perfect timing strategy. I’m interested in something less exciting but far more reliable: systematic thinking applied to volatile markets.

Finrev and its future as HyperTrend isn’t just another bot. It’s what happens when institutional quant research, HFT execution infrastructure, and a survival-first philosophy converge in decentralized finance. It’s the “bastard child” of a hedge fund and a high-frequency trading operation, and it’s built on a foundation of strategies that have worked across every asset class for over a century.

The research is rigorous. The team is credentialed. The track record is transparent, including the drawdowns and the long periods where nothing happens and what they are doing about that. And my role is to evaluate all of it independently, systematically, and honestly.

If you value data over drama, math over magic beans, and systematic thinking over emotional impulses, you’re in the right place.

Before trusting any trading system, verify:

- Methodology: Are strategies proven across decades in traditional markets? Or invented last month?

- Team: Institutional backgrounds (BlackRock, Jane Street, etc.) or self-taught with no track record?

- Transparency: Live results with drawdowns documented? Or just backtests and cherry-picked wins?

- Risk management: Honest about 6-12 month flat periods? Or promises consistent returns?

- On-chain verification: Can you verify every trade yourself? Or “trust us”?

If a system fails any of these checks: Be skeptical. If it passes all five: Worth deeper evaluation.

If you are interested, watch this Introduction Video with Scott Phillips, HyperTrend CEO At the end of the video, you will be invited to book a call with the onboarding team to explore whether this approach fits your risk tolerance and investment goals. They’ll walk you through the research, the track record, and the realistic expectations—no hype, no promises, no obligation, just the mathematics of professional-grade trading adapted for crypto. Your call will be handled by one of the experienced traders on their support team.

📄 Full Podcast Transcript: Algorithmic Survival in the Crypto Dark Forest

Questions or feedback? Reach me at contact@systematiccryptoresearch.com or via the contact form on this site. I am happy to respond and interested in hearing about your trading journey.

Disclosure: This article discusses Finrev and HyperTrend systems. The author may have positions in the mentioned assets. This is educational content, not financial advice. Crypto trading involves substantial risk of loss. Past performance doesn’t guarantee future results. Team backgrounds and credentials don’t guarantee trading system performance. Do your own research and verify all claims independently.