Ridge Optimization in Crypto Trading: Adaptive Signal System or Over-fitting Trap?

This podcast debate transcript accompanies the pillar article on Ridge multivariable optimization and the HyperTrend signal architecture. The counterarguments this episode examines are the ones most technically serious: that a soup of 100 signals is dangerously close to over-fitting, that black box algorithms blow up just as reliably as discretionary traders, and that the 365-day asset seasoning rule — while disciplined — may structurally miss the largest gains of any new market cycle.

“For the full signal architecture behind the HyperTrend algorithm — including the Ridge optimization methodology, Dark Forest execution, and the 8.46% maximum drawdown through the FTX collapse — read the pillar article this debate examines.”

⚡ Listen to the 04 Podcast on Spotify

Podcast Episode: 04 – The Complex Adaptive System Approach

Duration: ~17 minutes

Published: February 2026

Topic: How institutional algorithms navigate market regimes through Ridge optimization and predator-aware execution

📻 About This Podcast

This podcast transcript was generated using Google’s NotebookLM from the research in this article. The conversational debate format explores the concepts from multiple perspectives—examining both advantages and potential concerns—which can help clarify complex ideas that might be dense in written form.

This is a supplementary tool. The article contains the full technical analysis and primary sources. The podcast is for those who prefer audio learning or want to hear counterarguments explored through discussion.

📖 Read the Full Article: The Math Behind the Moonshots: Why Professional Research is the Only Way to Survive Automated Crypto Trading

⚡ What This Debate Revealed That the Article Didn’t Cover

The article makes the case for systematic algorithmic trading. The debate surfaces three challenges from the independent investor perspective that the systematic case doesn’t fully address:

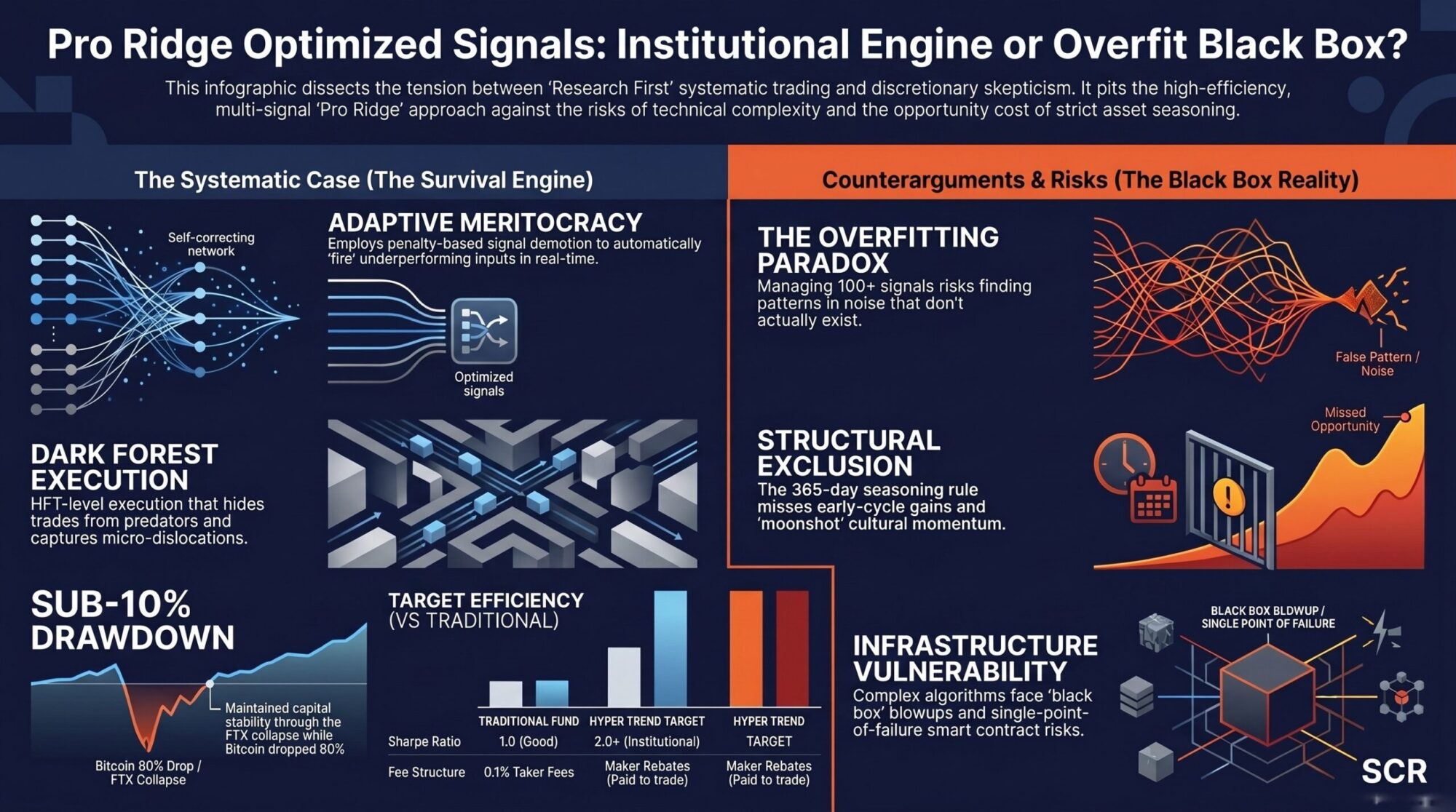

- A soup of 100 signals sounds dangerously like overfitting. The Expert’s overfitting challenge is the most technically serious pushback in the episode — and it deserves a better answer than the pillar article provides. The Ridge regression penalty for complexity is the real answer: it’s specifically designed to prevent over-weighting any single variable unless the evidence is overwhelming. But this distinction between a rigid 100-signal bot and a Ridge-weighted adaptive system is not obvious and most retail investors will miss it.

- Black box algorithms blow up too. The Expert’s opening position — “I’ve seen the black box algorithms blow up just as often as the discretionary traders” — is historically accurate and can’t be dismissed. The debate’s honest response is that the 10% max drawdown during Bitcoin’s 80% collapse is the empirical counter-argument, not a theoretical one. The system’s survival track record through the FTX collapse is the only meaningful evidence here.

- The 365-day seasoning rule will miss the biggest gains of the next cycle. The Expert’s final pushback — that the asset seasoning rule will miss 10x launches — is correct and acknowledged honestly. The systematic response is equally honest: yes, you’ll miss the top 1% of mania gains, but you’ll also miss the 90% collapse that follows. This trade-off is never discussed in the pillar article and the debate makes it explicit.

🧠 SCR Analysis: Where the Debate Lands

The Expert’s closing position in this episode is the most intellectually honest landing point in the series: “I’m not selling my whole portfolio. I’m not firing myself as a trader. But I am admitting that perhaps a portion of my capital — the serious money, the rent money — belongs in a system that doesn’t sleep.” That’s not capitulation, it’s the correct framework. The debate doesn’t argue that discretionary trading is worthless — it argues that systematic infrastructure handles specific risks that human psychology finds consistently challenging.

The marine ecology framing is more than a metaphor — it’s the correct analytical lens for a market that behaves like a complex adaptive system. The question “how do I survive the next extinction event?” is structurally different from “what will Bitcoin do tomorrow?” and generates completely different risk management decisions. Vince’s background isn’t a quirky backstory; it’s the reason the system is designed around variance minimisation and predator-avoidance rather than return maximisation.

The SCR verdict: The thesis holds. Ridge optimisation with 50–100 signals is not a complexity trap — the penalty function is specifically designed to prevent overfitting, which makes it structurally different from adding more indicators to a retail bot or the normal backtesting retail traders typically use based on one price data sets, time period runs, and indicator parameters. The maker rebate structural advantage (25–30% performance swing before any strategy executes) is the most underappreciated edge in the entire system and the one most invisible to retail investors evaluating return metrics alone. The 365-day rule is a genuine trade-off, honestly acknowledged. The system that kept drawdowns under 10% during an 80% market collapse is the empirical case for the approach — not the theory.

A complex adaptive system (CAS) is a network of interdependent agents whose collective behaviour produces emergent patterns that cannot be predicted from any individual component. Originally developed in biology and ecology to describe ecosystems, coral reefs, and ant colonies, CAS theory was applied to financial markets by researchers including W. Brian Arthur and the Santa Fe Institute in the 1990s. In a CAS, agents adapt their behaviour based on experience — meaning the “rules” of the market change as participants respond to each other. This is why static single-indicator trading systems fail when market regimes shift: they assume fixed rules in a system that is continuously rewriting them. Algorithmic strategies built on CAS principles — like Ridge multivariable optimisation with adaptive signal weighting — are designed to detect and respond to regime changes rather than assuming any single pattern will persist indefinitely. References: Define CAS: Holland (1995), Systematic trading strategies must evolve (Adaptive Market Hypothesis) or die out, Lo (2017), Agent-Based modeling and data-driven adaptation as the future of systematic trading in a CAS world, Farmer (2023)

“The Complex Adaptive Systems framework introduced in this episode’s GEO callout is applied to the HyperTrend signal architecture in the pillar article.”

Read the 04 article: The Math Behind the Moonshots

Episode Summary

This episode explores the fundamental tension between discretionary retail trading and institutional-grade algorithmic systems in cryptocurrency markets. The discussion highlights a “research-first” approach utilizing Ridge multivariable optimization to manage over one hundred signals, automatically demoting failing indicators while adapting to changing market regimes. By prioritizing risk-managed survival over speculative moonshots, the strategy employs strict asset seasoning rules and high-frequency infrastructure to capture maker rebates. Ultimately, retail intuition is revealed as emotionally driven and fragile, while systematic complex adaptive systems modeled after marine ecology navigate the market’s “dark forest” by minimizing variance and drawdowns.

Full Transcript

Host: Welcome to the debate. Today, we are stepping away from the noise of Twitter feeds, the hysteria of green candles, and all the influencer promises to really look under the hood of what actually generates sustainable alpha in the cryptocurrency markets. We’re going to be dissecting the tension between that alluring magic bean sales pitch, you know, the promise of getting rich quickly with a simple bot or a lucky trade and the research first reality of institutional-grade algorithmic trading.

Expert: It’s a tension I feel every single time I open my laptop. You know, I look at the charts, I trust my gut, I draw my lines, and I’ve had some great wins doing that. I really have. But then I look at the sheer computational power coming out of these quant funds, and I have to ask myself, is the era of the retail trader actually over? Can a guy with a laptop and some intuition really survive, or do we all just need to, I don’t know, bow down to the multivariable optimization gods and admit defeat?

Host: That is exactly the question we need to answer. I’m representing the systematic approach today. The Trader Army perspective, let’s call it, backed by physics PhDs and ex-BlackRock quants. My argument is that the market is a complex adaptive system where human emotion and simple static indicators are not just insufficient. They are active liabilities that will eventually destroy your capital.

Expert: And I’m here representing the independent investor, the guy in the trenches. I’ve seen the black box algorithms blow up just as often as the discretionary traders. So, I’m sceptical of over-complexity, and I’m wary of anything I can’t explain in plain English to my neighbour. I believe there is still value in the human element, the ability to, you know, read the room in a way that a machine just can’t. But I am open to being convinced, provided you can explain it without completely drowning me in math.

Host: Then, let’s begin. I want to start with a concept that really defines the systematic approach. Research first, hype never. If you look at the landscape of retail trading tools, it’s littered with corpses. Why? Because most of these retail bots, they’re built on really fragile foundations. They rely on single indicators, an RSI divergence, a moving average crossover, maybe a Bollinger band breakout, that kind of thing. They work beautifully in a backtest, and they might even work for a month in a strong bull market. But the moment the market regime changes, that single indicator just stops working. And because the bot has no brain, it keeps trading that broken signal until the account is empty.

Expert: I see why you think that, but let me give you a different perspective. A simple tool in the hands of a skilled craftsman is still very effective. You don’t need a laser-guided saw to build a table. If I see a moving average crossover in a strong trend, that’s a valid signal. It’s not fragile if it’s being managed by a human who knows when to turn it off. I know when the market is chopping, I just turn the bot off.

Host: But that “knowing when to turn it off” is exactly where the human fails. You sleep. You have emotions. You hesitate. The systematic answer to this is the HyperTrend strategy. It doesn’t rely on a single tool. It relies on a framework called Ridge multivariable optimization. So think of it not as a single hammer, but as a blended soup of say 50 to 100 different signals. You have volume predictors, hourly reversals, carry systems, and lead-lag correlations. The system isn’t betting on one thing happening. It is constantly listening to a hundred different inputs and weighing them based on what is working right now.

Expert: Okay, hold on. You’re throwing a lot of jargon at me there. Carry systems, lead-lag correlations. That sounds like a great way to sound smart while, you know, losing money. Break that down for me. What does a carry system actually look for in a crypto market?

Host: Fair point. Let’s look at the carry component. So, in crypto, you have perpetual futures. When the market is incredibly bullish, traders pay a fee, the funding rate, to keep their long positions open. A carry system just looks at those rates. If the crowd is paying these exorbitant fees to be long, the system might take the other side to capture those fees. Or it might identify that the cost of holding the position is just eating the profit. It’s profiting from the market’s expensive optimism. A simple moving average bot, well, it ignores that entirely.

Expert: Okay, I follow that. It’s looking at the cost of money, not just the price. What about lead-lag? That sounds like some kind of latency arbitrage.

Host: It’s simpler than that, but still very powerful. Historically, different assets are correlated. For a long time, if Ethereum moved, well, Solana might move 10 minutes later, or if Bitcoin dropped, the altcoin market would follow with a specific delay. The lead-lag signals in the soup are constantly measuring these correlations. So if Bitcoin spikes, the system asks, okay, based on the last week of data, does this predict a move in SOL? If the correlation is strong, it buys SOL before the retail crowd can even react.

Expert: Right? But those correlations break all the time. In 2021, everything moved together. In 2023, Bitcoin ran and alts just bled. If your system is betting on a correlation that breaks, you lose.

Host: Precisely. And that is why we use Ridge multivariable optimization. This is the key difference between a bot and an algorithm. It’s a meritocracy. The system is constantly grading its own homework. If the lead-lag signal starts failing, if Bitcoin moves and Solana doesn’t follow, the algorithm automatically demotes that signal. It just turns down the volume on the liar.

Expert: So it’s essentially firing the employees that aren’t performing.

Host: Exactly. In a complex system, you need an algorithm where signals that work get promoted and signals that fail get demoted automatically. It’s adaptive. It asks “what is working now?” Unlike the retail bot which just insists on doing what worked yesterday.

Expert: I have to play devil’s advocate here. A soup of a hundred signals sounds dangerously like overfitting to me. I mean, if you throw enough data points at a wall, you can make a chart look like anything you want. You’re telling me you need a hundred variables just to decide whether to go long on Bitcoin? Isn’t there a risk that the system is just finding patterns in the noise that don’t actually exist?

Host: That is the biggest risk in quantitative finance, and it’s why the “ridge” part of ridge regression matters. Without getting too deep into the math, Ridge regression basically applies a penalty to complexity. It actively resists giving too much weight to any single variable unless the evidence is just overwhelming. It is designed specifically to prevent overfitting. It prefers a soup of many small edges over one giant risky bet.

Expert: I’m listening, but I still feel like this takes the soul out of trading. I’ve seen these magic bean pitches, the flashy cars, the promises of retiring by Tuesday. Your pitch is the complete opposite. It’s the “trust me, I’m a doctor” pitch. Why do we need physics PhDs to buy an asset that historically just goes up if you hold it long enough?

Host: Because holding it long enough includes holding it through 80% drawdowns. And statistically, almost no retail investor actually holds through that. They panic sell at the bottom because they don’t have a mathematical framework to define risk. They just see their savings evaporating. The PhDs aren’t there to predict the future. They are there to engineer survival so you are actually still holding the asset when it recovers.

Expert: You keep using that word survival. You make trading sound like, I don’t know, natural selection in the jungle.

Host: That isn’t an accident. The lead researcher on this, Vince, he isn’t a traditional financier. He’s a marine ecologist.

Expert: A marine ecologist. Okay, now you’re losing me. We’re talking about high-frequency trading and digital assets. And your lead researcher is a guy who spent his career counting fish. What does a coral reef have to do with Bitcoin?

Host: It turns out almost everything. Vince views the market through the lens of complex adaptive systems. Think about a coral reef. It is a massive interconnected system. You have predators, prey, environmental cycles, temperature shifts. It looks chaotic, but it is governed by rules. A crypto exchange is exactly the same. It has whales, retail plankton, liquidity flows, and of course, panic cycles.

Expert: So Vince is treating the market like an ecosystem, not a game.

Host: Precisely. And when you view it that way, the question isn’t “what will Bitcoin do tomorrow?” The question is “how do I survive the next extinction event?” Most retail traders are trying to be apex predators, but they’re actually prey. Vince’s systems are designed to be generalist survivors. They don’t need any one thing to work. They just need to be alive when the dust settles.

Expert: That’s a sobering way to think about it. Okay, so if we’re designing for survival, what does that look like in practice? What actual rules does the system follow?

Host: One of the most critical is the 365-day rule. The system will not touch an asset unless it has at least one full year of tradable history.

Expert: Wait, so if some hot new token launches and it goes 10x in a month, you just sit there and watch?

Host: Yes. And that discipline is what keeps you alive. Think about how many of those 10x tokens are at zero six months later. Luna, FTX token, hundreds of others. The year requirement filters out the garbage. By the time an asset has survived 365 days, you know it has liquidity, you know it has market makers, you know it can survive volatility.

Expert: I can respect the discipline even if it hurts my degenerate soul. But let’s pivot to the mechanics. You mentioned earlier that slow signals beat fast ones because of fees. But then I read about your infrastructure and it sounds like you’re trying to be a high-frequency trader. Which is it? Slow and steady or fast and furious?

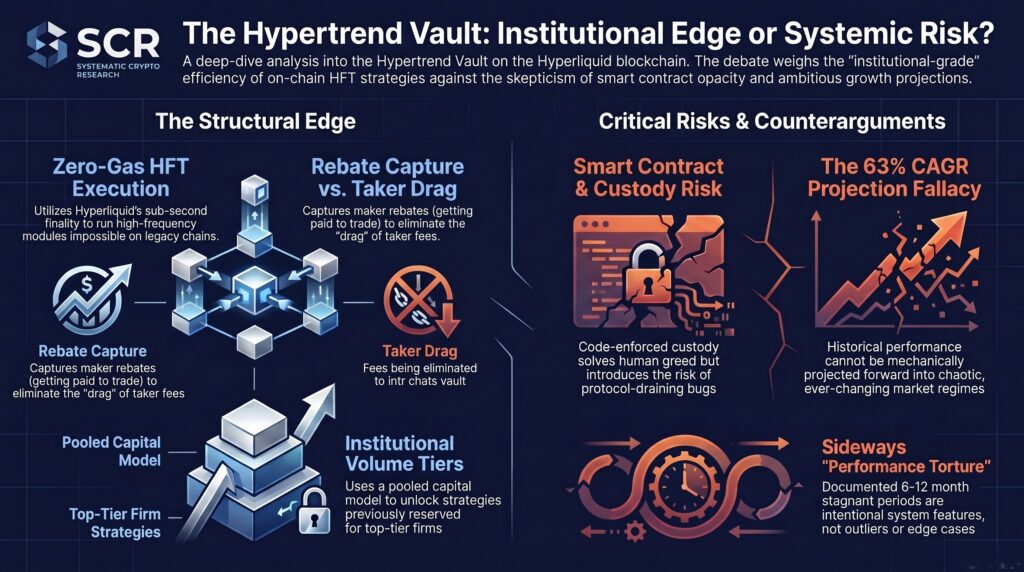

Host: It’s a hybrid. And this brings us to the infrastructure, specifically the Hyperliquid vault system. This is where the retail trader gets completely left behind. In the old model, if you ran a bot on your laptop connected to an exchange, you paid a taker fee every time you executed a trade. Maybe 0.1%.

Expert: Right? That’s just the cost of doing business for retail.

Host: Yes. But the HyperTrend system operates within a vault that pools capital to reach the highest volume tiers. It doesn’t pay fees. It collects maker rebates.

Expert: Explain that. You get paid to trade?

Host: Yes. When you place a limit order that adds liquidity to the book, meaning you aren’t taking a price instantly, but offering a price, the exchange pays you. It’s a rebate.

Expert: How much of a difference does that actually make?

Host: It is massive. For a retail trader, fees might eat 20 or even 30% of your annual profits depending on how much you trade. In this system, rebates might add 5% to the bottom line. That is a 25 or 30% swing in performance just based on infrastructure. You start every single trade with a mathematical head start.

Expert: Okay. That is a real edge. I can’t argue with negative fees. That’s the casino paying you to sit at the table.

Host: Exactly. And it goes deeper. The system has partnered with Dark Forest Technology to handle the execution.

Expert: Dark Forest sounds ominous.

Host: It’s an engineering metaphor. The dark forest of crypto is the mempool. The place where pending transactions wait to be confirmed. Predatory bots watch this forest. If they see you trying to buy a large amount, they front-run you. They buy just before you, push the price up, and then sell it back to you.

Expert: Yeah, I’ve been sandwiched by those bots. It’s infuriating.

Host: So, Dark Forest Technology allows for HFT level execution that hides from those predators and even exploits micro-dislocations. Think of the system as a genetic hybrid. It takes the patience of a trend following fund, that soup we talked about, and it splices it with the execution speed of a high-frequency trading firm.

Expert: So it decides what to buy slowly but executes the buy at the speed of light.

Host: Precisely. It captures edges that are completely invisible to the naked eye. For example, if the price of Bitcoin is $100,000 on Binance and $100,050 on Coinbase, a human can’t click fast enough to arbitrage that. The system can.

Expert: Okay, please don’t use any more genetic metaphors. It’s getting weird. But I get the point. You’re saying the game is rigged and the only way to win is to join the people rigging it.

Host: I would say the game has evolved. You can try to hunt with a spear, your manual charts and intuition, or you can join the team using satellite tracking and automated drones.

Expert: It makes me feel like I’m bringing a knife to a nuclear war, but I have to push back one last time. You talk about safety and rebates and variance. But what about the black swan you can’t model? What about exchange risk? What about a bug in the code? If I trade manually, I hold my own keys. If I put my money in your vault, isn’t that a massive single point of failure?

Host: That is a valid concern and it is the trade-off of any institutional approach. You are trusting the infrastructure. However, the Hyperliquid vault is on-chain. It’s transparent. But yes, there is smart contract risk, there is platform risk. That is why “research first” applies to where you put your money, not just what you buy.

Expert: At least you admit it. There is no such thing as a risk-free lunch.

Host: Never. Only risk-managed lunches.

Expert: Let’s wrap this up. I’m listening to you and I’m looking at my own portfolio. I love the thrill. I love the hunt for the moonshot. I don’t think I can ever fully give that up. There is a dopamine hit in hitting that buy button and being right that an algorithm can never replace. And frankly, I think your 365-day rule is going to miss the biggest gains of the next cycle.

Host: You might be right. We will miss the top 1% of the mania, but we will also miss the 90% drop that follows.

Expert: I have to concede that the math behind the strategy is terrifyingly sound. The idea of competing against a system that eats micro-dislocations for breakfast and gets paid rebates to do it, it’s sobering. I think I’m adopting a curious stance here. I’m not selling my whole portfolio. I’m not firing myself as a trader. But I am admitting that perhaps a portion of my capital, the serious money, the rent money, belongs in a system that doesn’t sleep.

Host: And that is a wise approach. We are not asking for blind faith. We are asking for a recognition of limitations. Humans are terrible at systematic trading. We are wired for survival on the savannah running from lions, not for calculating probability theory in financial markets.

Expert: Speak for yourself. I’m great on the Savannah.

Host: I’m sure you are. But James Hodges and Scott Phillips, the Trader Army, they didn’t build a gambling bot. They built a survival engine. You mentioned drawdowns earlier. It’s worth reminding everyone when Bitcoin had its 80% drawdowns, this system during its testing phases, including the FTX collapse, kept drawdowns under 10%.

Expert: That is the stat that sticks with me. 80% versus 10%. That’s the difference between ruin and a bad month.

Host: It is. And that is why we say “research first, hype never.” Whether you trade manually or automatically, you must respect the data.

Expert: Well, you’ve given me a lot to think about. I might still buy a few magic beans tomorrow, but I might put them in a separate jar from the serious money. And I’ll try not to think about the dark forest waiting to eat me.

Host: Just remember, in the dark forest, it pays to be the one with the map.

Expert: Touché.

Host: For our listeners, remember the market is a complex ocean. You can swim alone or you can bring a submarine. Choose wisely. This has been the debate.

📖 Read the Full Article: The Math Behind the Moonshots: Why Professional Research is the Only Way to Survive Automated Crypto Trading

Key Takeaways

- Ridge Optimization Prevents Single-Point-of-Failure Trading – Unlike retail bots relying on one indicator, Ridge multivariable optimization manages 50-100 uncorrelated signals, automatically demoting failures and promoting what works now.

- Market Regimes Change, Static Indicators Don’t – What works in bull markets (moving average crossovers) fails in choppy conditions. Complex adaptive systems adjust weights dynamically rather than insisting on yesterday’s edge.

- The 365-Day Asset Seasoning Rule Filters Garbage – Refusing to trade assets with less than one year of history eliminates Luna-style implosions while accepting that you’ll miss some 10x moon shots.

- Maker Rebates Create 25-30% Performance Swing – Pooled capital reaching institutional volume tiers earns exchange rebates instead of paying taker fees, creating structural advantage before any strategy executes.

- Dark Forest Execution Hides from Predatory Bots – Front-running bots in the mempool sandwich retail orders. HFT-level execution with Dark Forest Technology exploits micro-dislocations while avoiding predator detection.

- Survival Engineering Beats Prediction – Marine ecology perspective: the question isn’t “what will Bitcoin do tomorrow?” but “how do I survive the next extinction event?” Generalist strategies outlast specialists.

🎯 Explore the Systematic Approach

The gap between retail intuition and institutional execution isn’t about being smarter — it’s about infrastructure, discipline, and mathematical frameworks for survival.

Next Step: Watch the introduction video to understand how Ridge optimization adapts to regime changes in real-time, the 365-day rule and other survival-focused filters, and why maker rebates and Dark Forest execution create structural edges.

The system kept drawdowns under 10% during Bitcoin’s 80% collapse. That’s the difference between extinction and evolution.

Resources Mentioned

- Ridge Multivariable Optimization – Algorithm that weights 50-100 signals while penalizing over-complexity

- Vince (Marine Ecologist) – Lead researcher applying complex adaptive systems theory to markets

- Dark Forest Technology – HFT execution partner preventing front-running and capturing micro-edges

- HyperTrend Vault – Pooled capital system on Hyperliquid earning maker rebates

- 365-Day Asset Rule – Minimum trading history requirement filtering new token disasters

- FINREV – Legacy system proving 10% max drawdown during 80% Bitcoin collapse

- James Hodges & Scott Phillips – Trader Army founders (ex-BlackRock quants and physics PhDs)

About This Podcast

This debate explores the fundamental tension between human intuition and algorithmic precision in crypto markets. For traders recognizing the limitations of manual execution and static indicators, understanding complex adaptive systems and institutional infrastructure separates survival from extinction.

Related Articles:

- Why a Proven Crypto Trading System is Rebuilding on Hyperliquid Vault Infrastructure

- Complex Adaptive Systems in Finance: What Marine Ecology Teaches About Market Survival

- The Death of Retail Bots: Why Single-Indicator Trading is Obsolete

Transcript generated from Notebook LM podcast discussion. Edited for clarity and formatted for web publication.